The RBI held the policy repo rate unchanged at 6.5% in its October 2023 MPC meeting, on expected lines and continued with its ‘withdrawal of accommodation’ stance. In the policy statement the Governor said, “The MPC remains highly alert and prepared to undertake timely policy measures, as may be necessary, in order to align inflation to the target and anchor inflation expectations”. Comments by the RBI governor in the post policy press conference too, suggest RBI’s preference for tighter liquidity conditions.

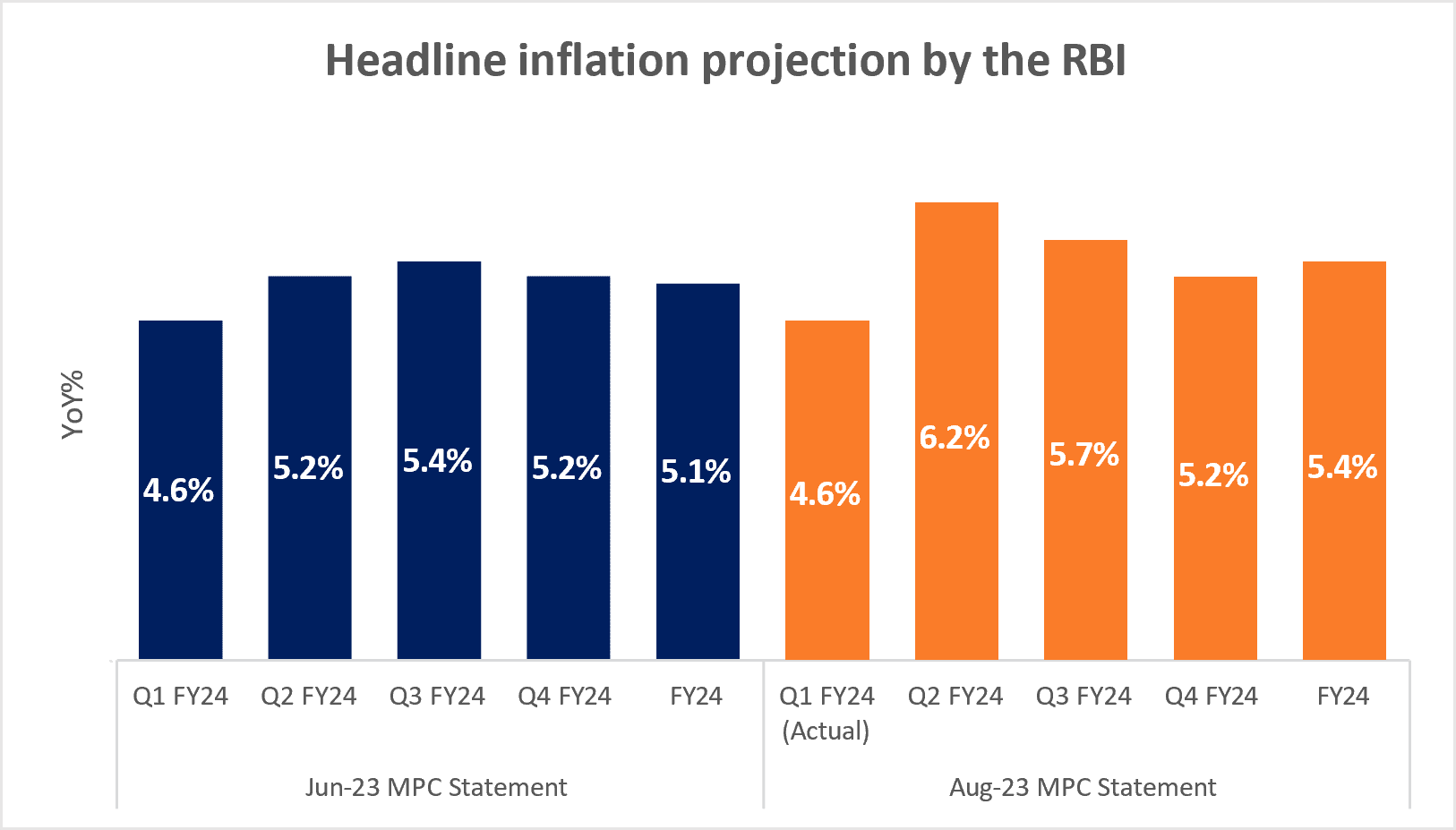

The RBI left the growth and inflation projections for FY24 unchanged at 6.5% and 5.4% respectively. Q2 FY24 inflation forecast has been revised slightly upwards to 6.4% from 6.2% earlier, while Q3 FY24 has been revised downwards to 5.6% from 5.7% earlier. On the domestic front risks to inflation stem primarily from elevated levels of food prices – fruits and vegetables, cereals, pulses and spices. On the global front, oil prices are up 30% over the last 2 months. The US dollar too, has strengthened by ~3% over the course of the last quarter, leading to a weaker rupee. Additionally, developed markets central banks are hinting at higher for longer interest rates.

The Governor stressed on the skewed liquidity situation in the banking system with banks preferring to place funds under the overnight SDF instead of the main 14-day variable rate reverse repo (VRRR) operations. The Governor also highlighted that borrowings under the MSF have remained high despite banks parking substantial funds under the SDF. To absorb the excess liquidity, the RBI in its August 10 policy statement introduced an incremental cash reserve ratio (I-CRR) of 10% which removed about ₹1.1 lakh crore from the banking system. The I-CRR is being withdrawn in a phased manner starting September 8, with complete withdrawal by October 7. Today’s statement suggests that the RBI will keep a close watch on the liquidity situation and actively mange it.

TheGovernorclarifiedthatOMOsalesarenottobeviewedasayieldmanagementtoolbutareintendedtomanageliquidity conditionsinresponsetodomesticconditions.However,G-secyieldsstilljumped15bpsinresponsetothepolicyannouncement. TherecentriseinglobaloilpricesisunlikelytohaveasignificantdirectimpactonCPI.GreaterriskstoCPIemanatefromfoodprices. TheRBIaimstoanchorinflationexpectationsat4%.HeadlineCPIinflationwillremainaboveRBI’scomfortzoneandis expectedto average ~5.5% inthefiscal.WefeeltheRBIwillmaintainstatus quointhe nextpolicymeetingaswell, unlessthings fall way outof place.

Skewed liquidity firms up weighted average call rates

Declining core inflation is a silver lining

Skewed liquidity firms up weighted average call rates

Declining core inflation is a silver lining

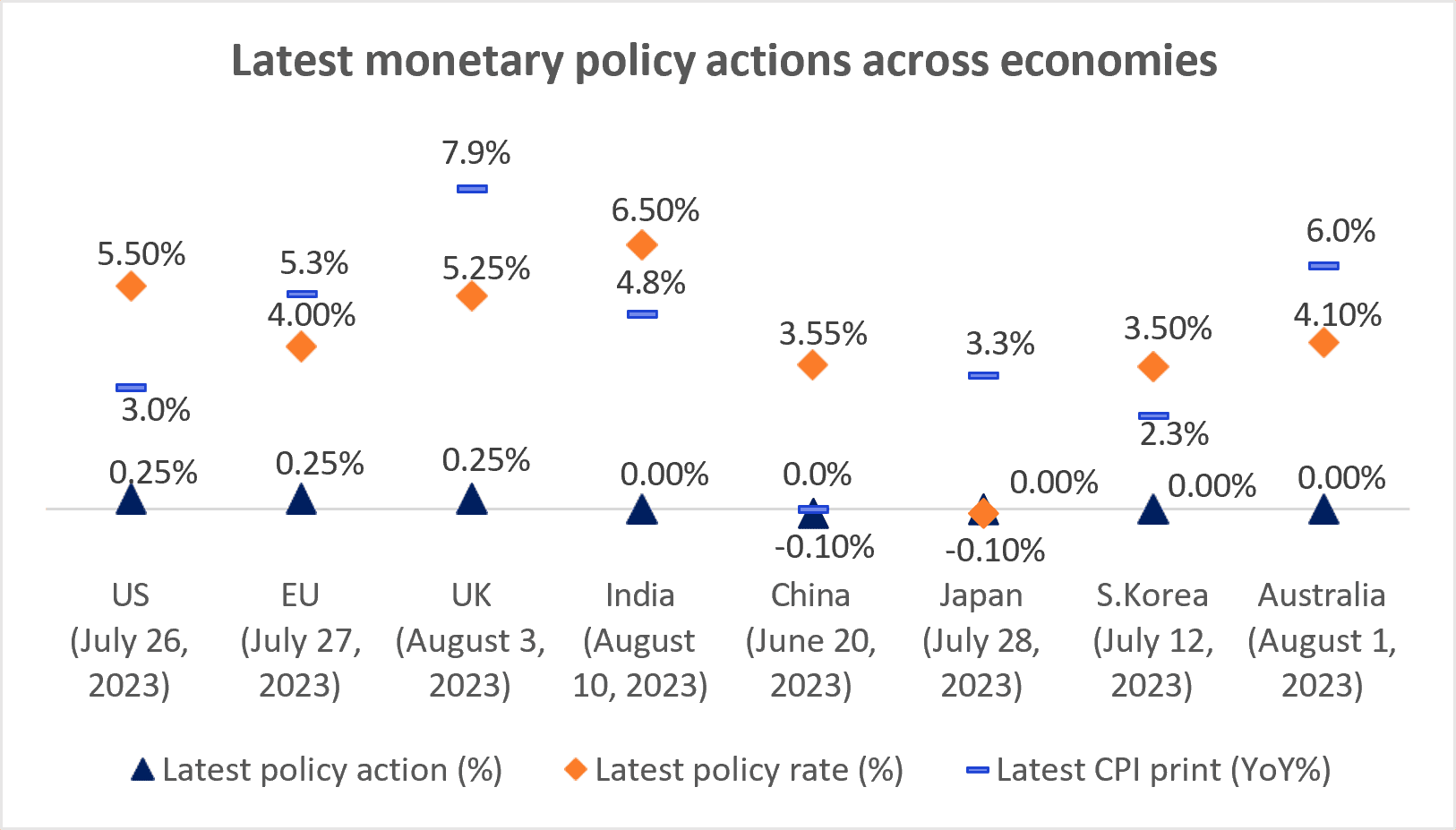

EU and UK still not off the rate hiking cycle

I-CRR being discontinued in a phased manner

EU and UK still not off the rate hiking cycle

I-CRR being discontinued in a phased manner

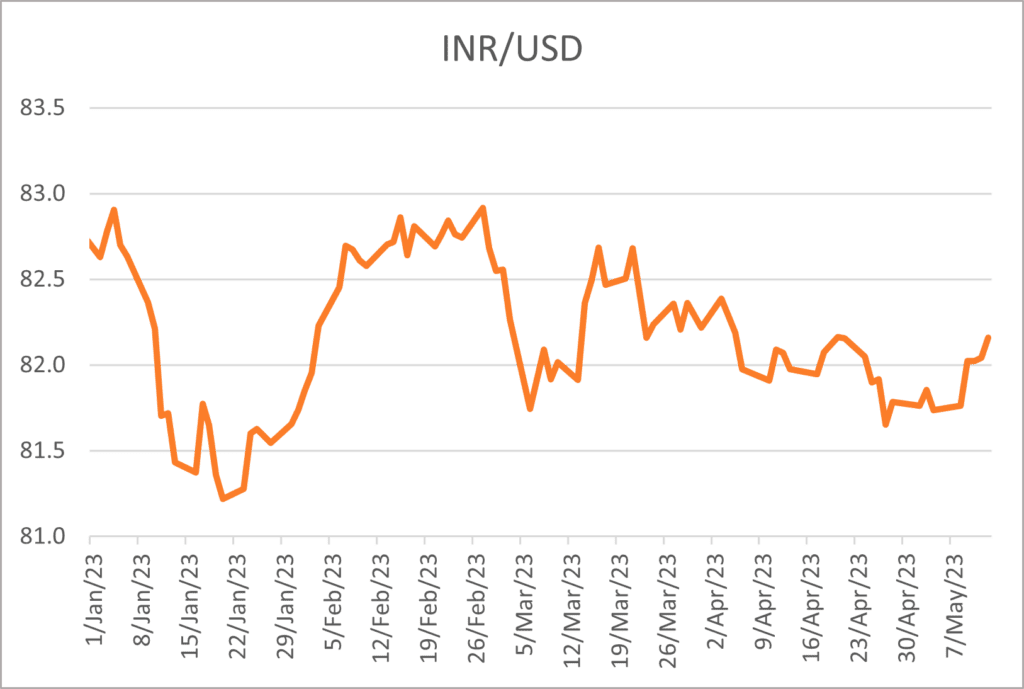

INR is among the better performing currencies in 2023 with low volatility

Falling REER signals an appreciating bias for

INR

INR is among the better performing currencies in 2023 with low volatility

Falling REER signals an appreciating bias for

INR

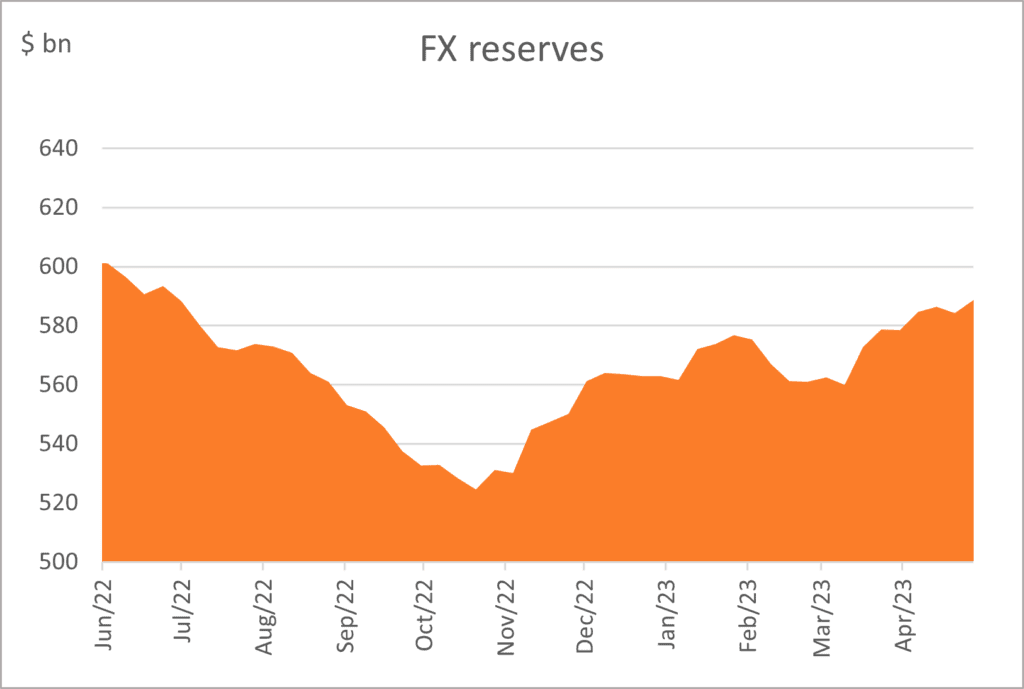

RBI has been shoring up its

reserves

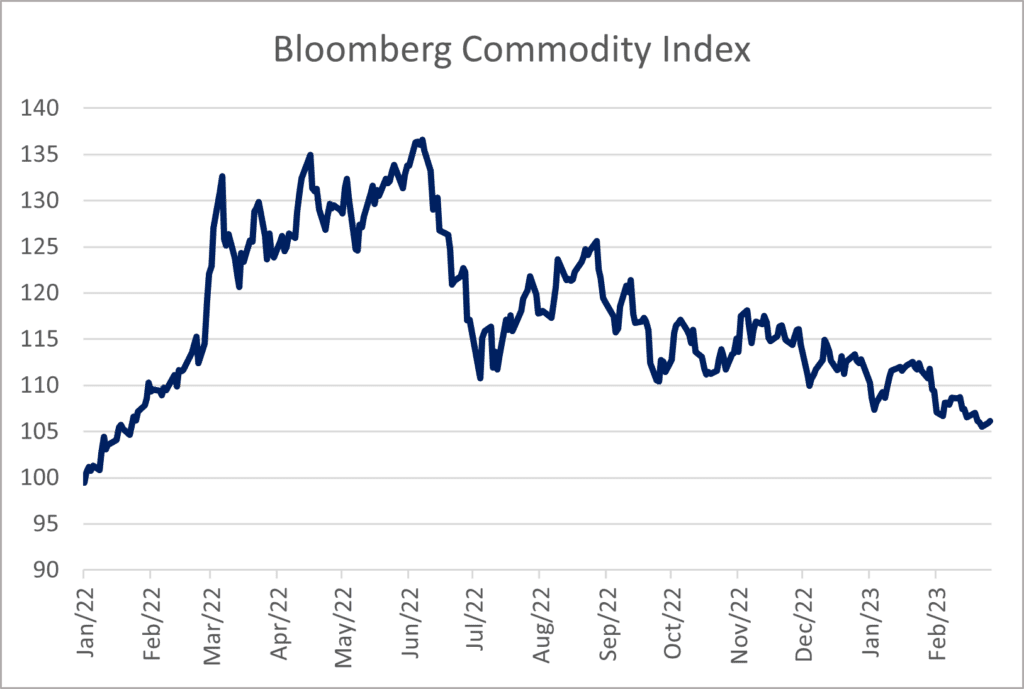

Commodity prices have been on a

downtrend

RBI has been shoring up its

reserves

Commodity prices have been on a

downtrend

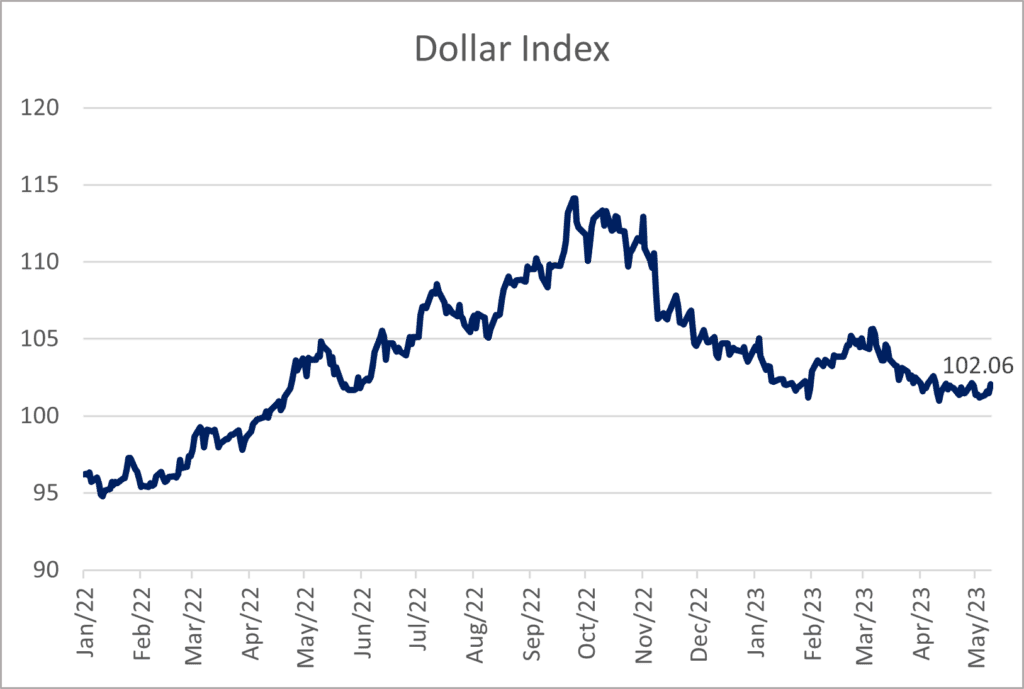

With a weak economic outlook and Fed pause, US dollar is losing its strength

CAD remains in a comfortable

position

Average retail mandi prices

With a weak economic outlook and Fed pause, US dollar is losing its strength

CAD remains in a comfortable

position

TruQuest is knowledge series launched by TruBoard Partners providing succinct updates and views on:

Liquidity outlook

India’s macro economic view

Trends within the infrastructure, Real Estate and Renewable Energy sectors

Impact analysis of new regulations and policies on lending and capital flow

Anuj Agarwal, Chief Economist Ria Rattanpal, Research Associate

Author:

Anuj Agarwal, Chief Economist Ria Rattanpal, Research Associate

Disclaimer

The data and analysis covered in this report of TruQuest has been compiled by TruBoard Pvt Ltd and its associates (TruBoard) based upon information available to the public and sources believed to be reliable. Though utmost care has been taken to ensure its accuracy, no representation or warranty, express or implied is made that it is accurate or complete. TruBoard has reviewed the data, so far as it includes current or historical information which is believed to be reliable, although its accuracy and completeness cannot be guaranteed. Information in certain instances consists of compilations and/or estimates representing TruBoard’s opinion based on statistical procedures, as TruBoard deems appropriate. Sources of information are not always under the control of TruBoard. TruBoard accepts no liability and will not be liable for any loss of damage arising directly or indirectly (including special, incidental, consequential, punitive or exemplary) from use of this data, howsoever arising, and including any loss, damage or expense arising from, but not limited to any defect, error, imperfection, fault, mistake or inaccuracy with this document, its content.