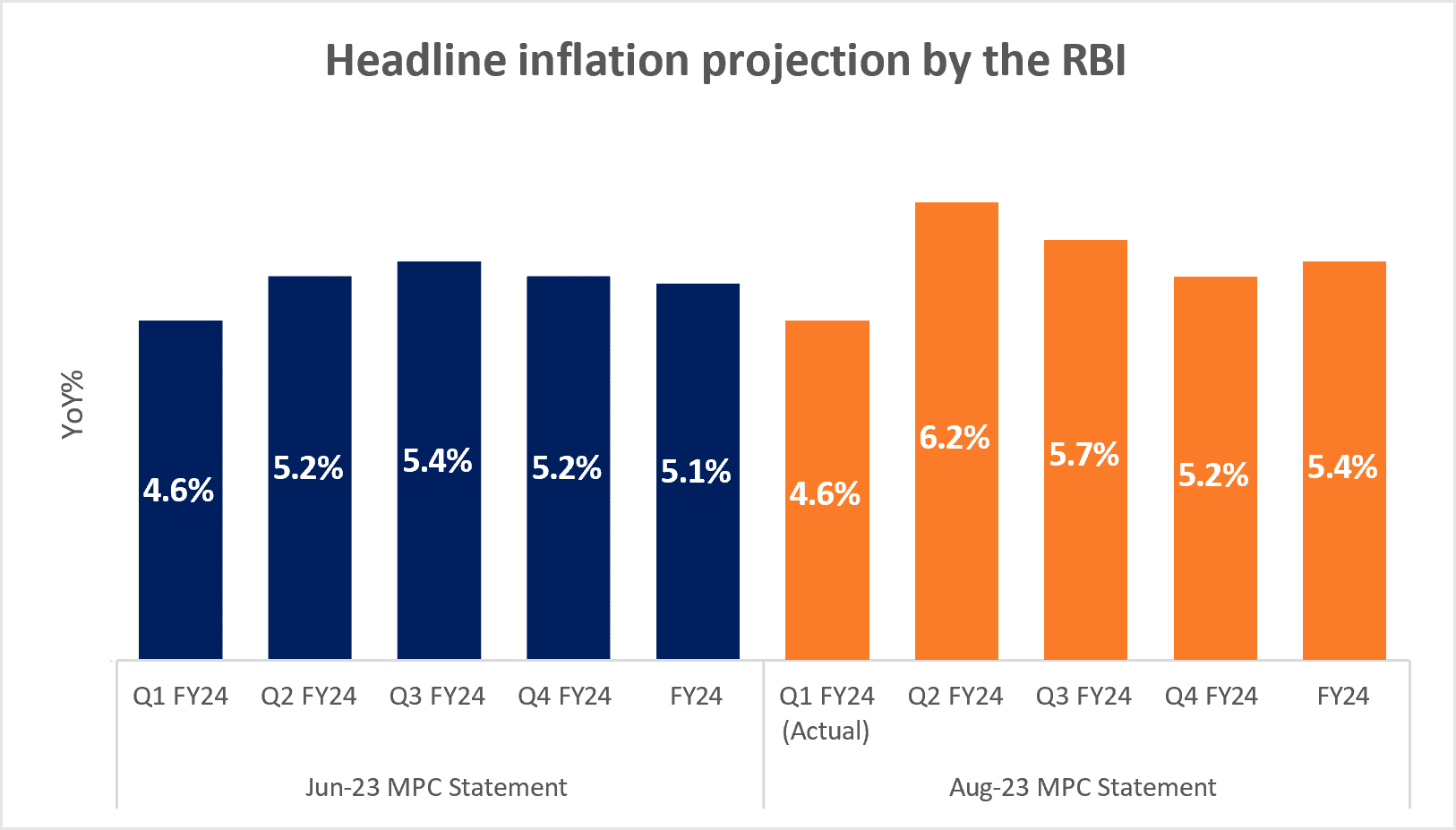

The RBI held the policy repo rate unchanged at 6.5% in its August 2023 MPC meeting, on expected lines. The Governor reiterated the RBI’s commitment to bring inflation down to 4% on a durable basis. The Governor said, “We do look through idiosyncratic shocks, but if such idiosyncrasies show signs of persistence, we have to act”. Buoyed by a spike in food prices, headline CPI print for July 2023, is likely to come in closer to 6%.

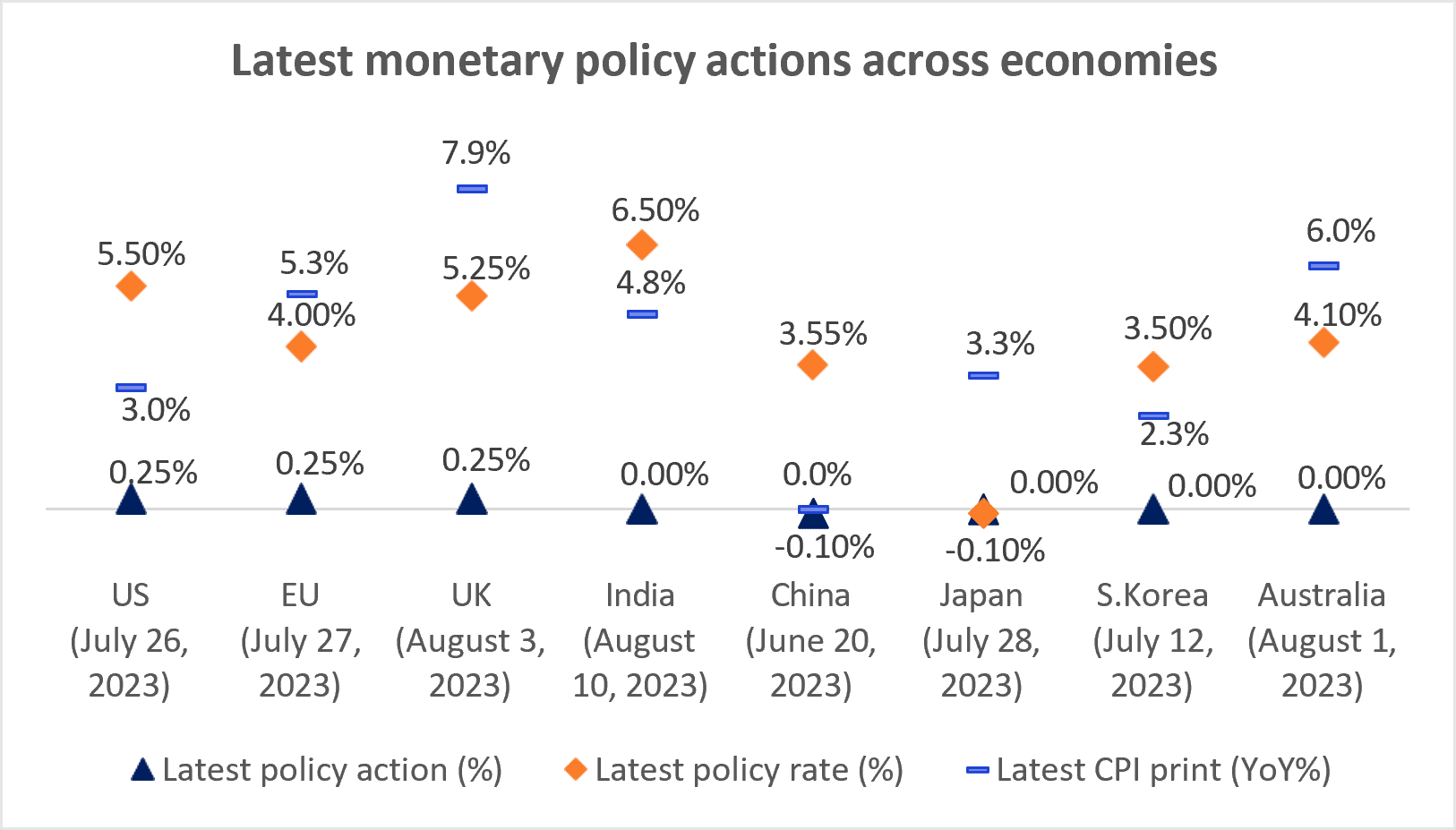

Food inflation remains elevated and high prints are concentrated in a few items – rice, atta, tomato, ginger, garlic, toor dal, dry chilli, jeera, ghee, salt, and coffee powder. These prices are expected to ease in the coming months. Vegetable prices have started to show some correction in the first week of August, compared to the preceding week. On the global front, geopolitical tensions have led to some hardening of food prices. Global oil prices too are up 12% in August compared to a month ago on concerns over tightness in the physical market. This, however, is unlikely to have a significant impact on headline CPI. The government has controlled the retail prices of petrol and diesel and kept them steady since last year.

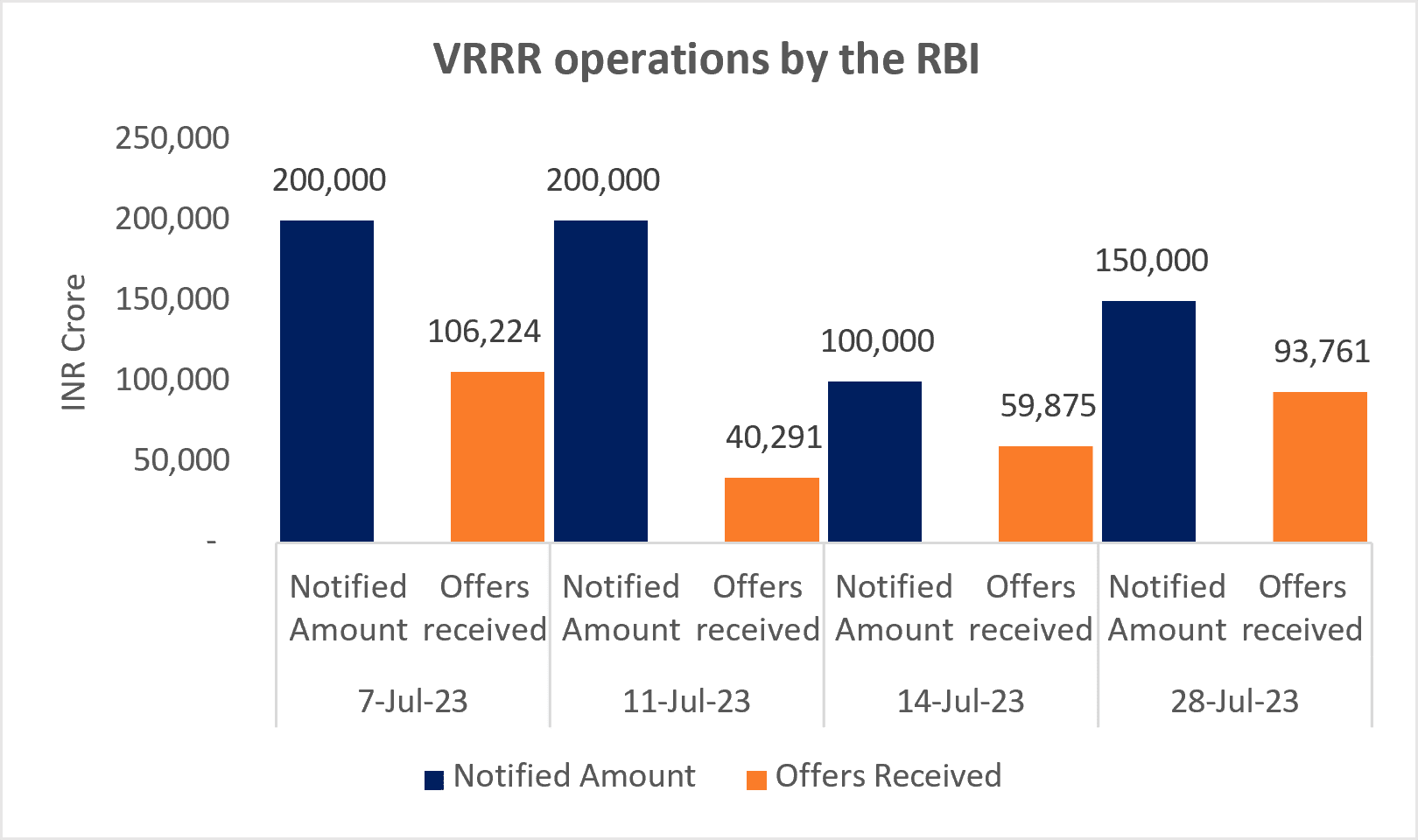

The Governor highlighted the concerns over the surplus liquidity in the system and the lukewarm repose to the VRRR auctions. To absorb the excess liquidity, the RBI has introduced a temporary measure of incremental cash reserve ratio (I- CRR) of 10% on the increase in banks’ net demand and time liabilities (NDTL) between May 19, 2023 and July 28, 2023. The CRR has been left unchanged at 4.5%.

Anuj Agarwal, Chief Economist Ria Rattanpal, Research Associate

Author:

Anuj Agarwal, Chief Economist Ria Rattanpal, Research Associate

Disclaimer

The data and analysis covered in this report of TruQuest has been compiled by TruBoard Pvt Ltd and its associates (TruBoard) based upon information available to the public and sources believed to be reliable. Though utmost care has been taken to ensure its accuracy, no representation or warranty, express or implied is made that it is accurate or complete. TruBoard has reviewed the data, so far as it includes current or historical information which is believed to be reliable, although its accuracy and completeness cannot be guaranteed. Information in certain instances consists of compilations and/or estimates representing TruBoard’s opinion based on statistical procedures, as TruBoard deems appropriate. Sources of information are not always under the control of TruBoard. TruBoard accepts no liability and will not be liable for any loss of damage arising directly or indirectly (including special, incidental, consequential, punitive or exemplary) from use of this data, howsoever arising, and including any loss, damage or expense arising from, but not limited to any defect, error, imperfection, fault, mistake or inaccuracy with this document, its content.