US Federal Funds Rate – Steady But Higher For Longer

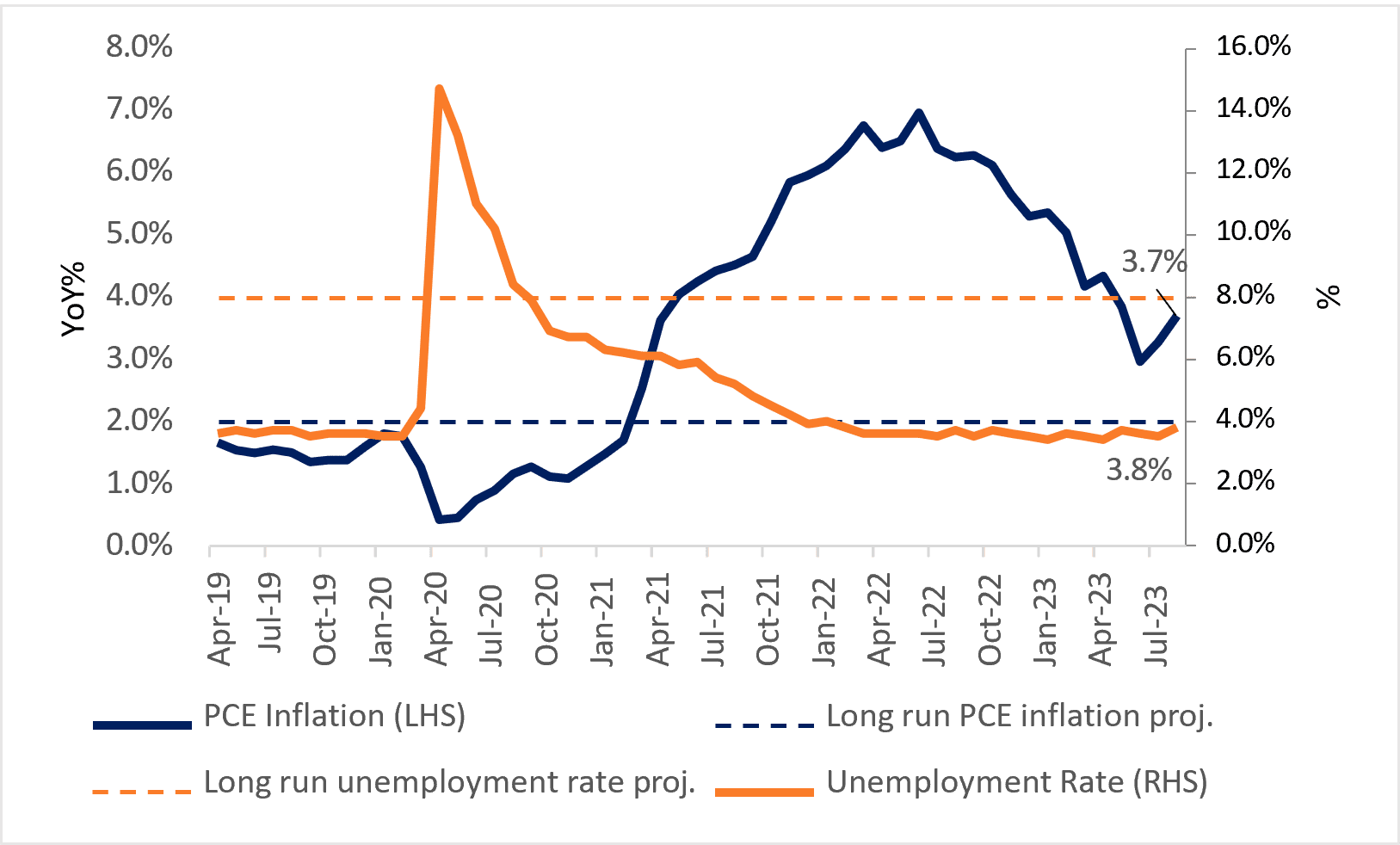

The US FOMC held rates steady on expected lines. The Fed’s September statement was on similar lines as June – strong economic activity, resilient banking system, tighter credit conditions with an uncertain impact, focus on bringing down inflation, and data dependent future actions. The committee left the door open for another hike this year. In the press conference, Fed Chair Powell said, “If the economy evolves as projected, the median participant projects that the appropriate level of the federal-funds rate will be 5.6% at the end of this year, 5.1% at the end of 2024, and 3.9% at the end of 2025.”

Revised projections by the Fed suggest that rates are likely to remain higher for longer. Federal funds rate projections for 2023 are unchanged from June at 5.6%. However, projections for 2024 are higher at 5.1% Vs 4.6% in June. 12 of 19 officials favor raising rates one more time in 2023. For 2026, while GDP growth, unemployment rate, and inflation are projected top reach long-run levels, Fed funds rate is projected at 2.9% which is higher than the long run rate of 2.5%. This suggests that FOMC members think that the neutral rate (which keeps inflation and unemployment stable over time) has risen.

The US economy has beaten expectations of a slowdown despite the consecutive rate hikes by the Fed. Projections by the Fed and performance of the US economy suggests that a soft-landing is very much achievable. Core PCE inflation has started showing signs of moderation, so have earnings growth. However, both unemployment and inflation remain above the Fed’s target. Brent crude oil prices are up 30% over the last two months crossing $95 a barrel, posing a renewed threat to inflation. From a future guidance point of view, it is easier for officials to project one more increase and then opt against it than to signal no more increases and then hike again. Fed officials are cautiously optimistic, with an emphasis on cautiously. We are of the opinion that the US FOMC will hold rates steady in November.

Projections signal a rate hike in 2023 and higher than earlier anticipated rates in 2024

Probabilities as on Sep 20

Probabilities as on Sep 21

Source : CME Fed Watch Tool, FRED, Fed, TruBoard

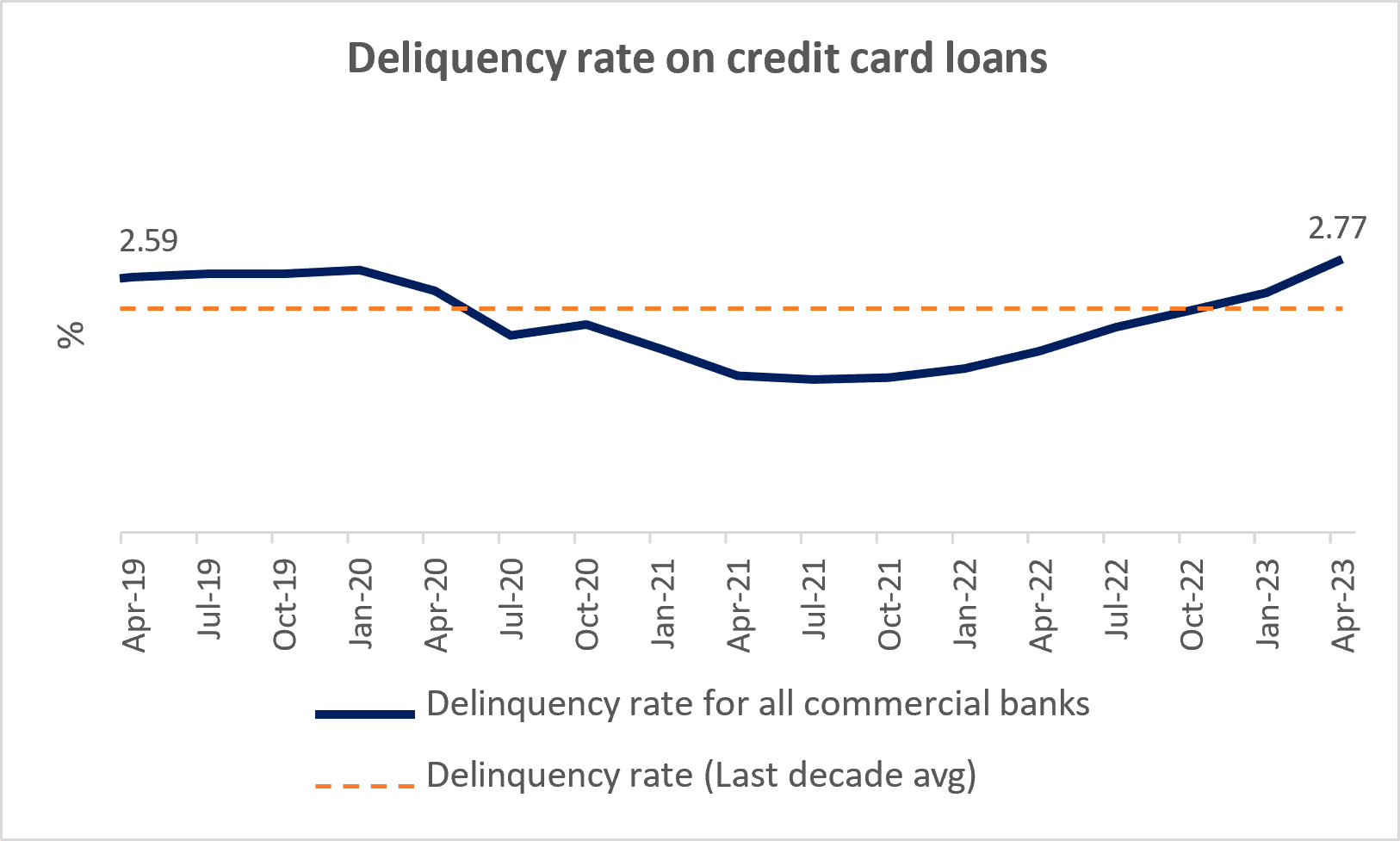

Average credit card interest rate at a record high at 20.6%

The data and analysis covered in this report of TruQuest has been compiled by TruBoard Pvt Ltd and its associates (TruBoard) based upon information available to the public and sources believed to be reliable. Though utmost care has been taken to ensure its accuracy, no representation or warranty, express or implied is made that it is accurate or complete. TruBoard has reviewed the data, so far as it includes current or historical information which is believed to be reliable, although its accuracy and completeness cannot be guaranteed. Information in certain instances consists of compilations and/or estimates representing TruBoard’s opinion based on statistical procedures, as TruBoard deems appropriate. Sources of information are not always under the control of TruBoard. TruBoard accepts no liability and will not be liable for any loss of damage arising directly or indirectly (including special, incidental, consequential, punitive or exemplary) from use of this data, howsoever arising, and including any loss, damage or expense arising from, but not limited to any defect, error, imperfection, fault, mistake or inaccuracy with this document, its content.