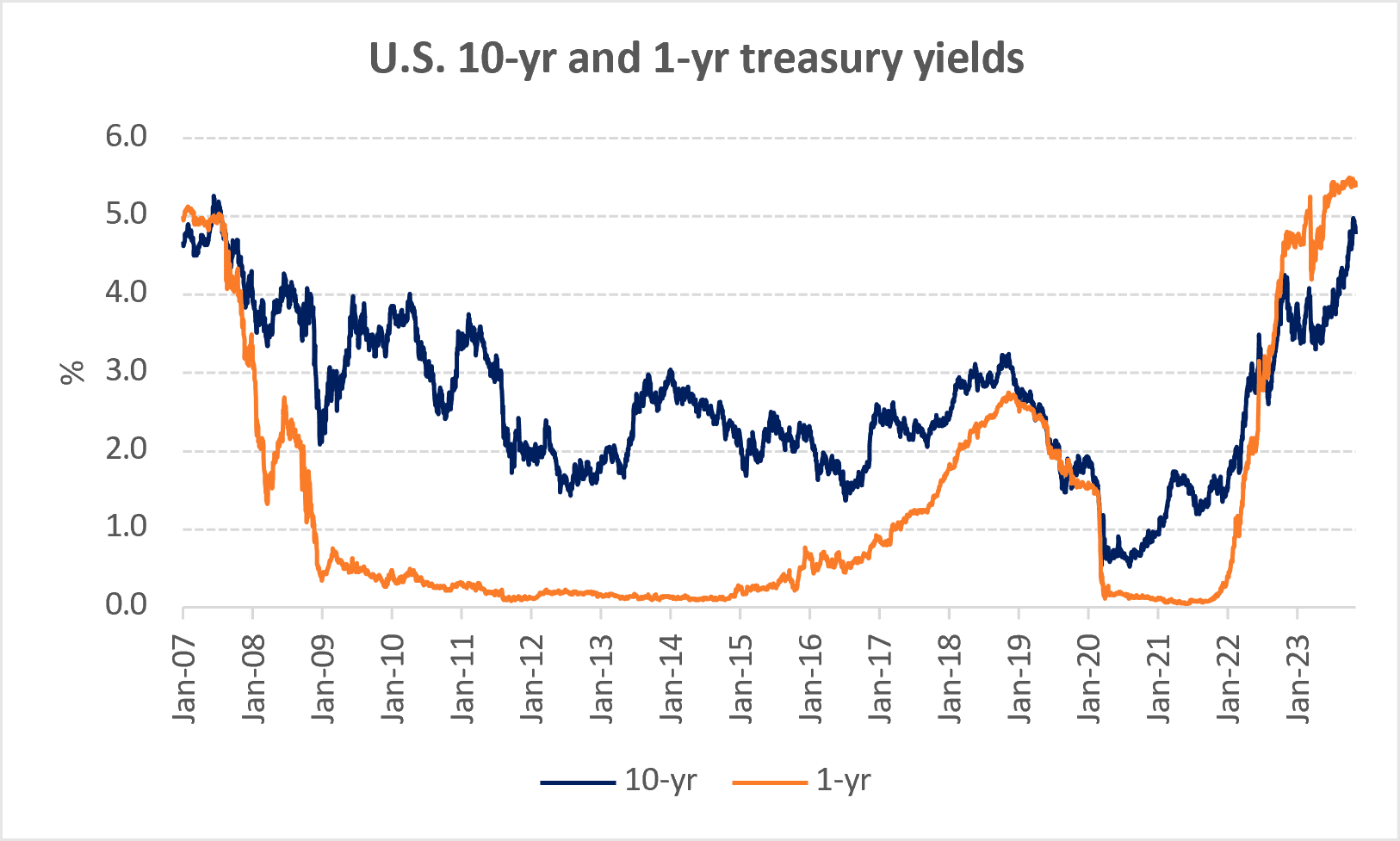

The U.S. FOMC held rates steady on expected lines. The tone of the statement was similar to the one in September – strong economic activity, resilient banking system, tighter credit conditions with an uncertain impact, focus on bringing down inflation, and data dependent future actions. However, while the September policy had strong hints of an additional rate hike in 2023, the November policy did not give any specific signal to this effect. The FOMC has held rates steady in a range of 5.25% to 5.5% since July 2023. U.S. inflation has moderated to 3.4% in September from a peak of 7.1% in June.

While the Fed adjusts short-term rates, it impacts the long-term rates with a lag. The 10-year U.S. Treasury yield (which forms the base for other interest rates in the market) has risen 100bps in less than three months and crossed 5% in October – for the first time since 2007. Fed Chair Powell acknowledged that monetary policy is restrictive, and its effects are visible. Higher rates will lead eventually lead to higher default rates for companies and individuals, weighing down on growth, which could push the economy away from a soft landing. The Fed chair acknowledged that the risks of doing too little to tackle inflation versus doing too much had become more “two-sided”. Inflation cooling off to 2% with rates remaining high would also suggest that the neutral rate has moved higher. This would provide ammunition to the Fed to act when recession hits.

The data and analysis covered in this report of TruQuest has been compiled by TruBoard Pvt Ltd and its associates (TruBoard) based upon information available to the public and sources believed to be reliable. Though utmost care has been taken to ensure its accuracy, no representation or warranty, express or implied is made that it is accurate or complete. TruBoard has reviewed the data, so far as it includes current or historical information which is believed to be reliable, although its accuracy and completeness cannot be guaranteed. Information in certain instances consists of compilations and/or estimates representing TruBoard’s opinion based on statistical procedures, as TruBoard deems appropriate. Sources of information are not always under the control of TruBoard. TruBoard accepts no liability and will not be liable for any loss of damage arising directly or indirectly (including special, incidental, consequential, punitive or exemplary) from use of this data, howsoever arising, and including any loss, damage or expense arising from, but not limited to any defect, error, imperfection, fault, mistake or inaccuracy with this document, its content.