The RBI held the policy repo rate unchanged at 6.5% in its December 2023 MPC meeting, on expected lines and continued with its ‘withdrawal of accommodation’ stance. The tone of the statement suggests that the RBI is happy with the developments in the economy – broad-based easing of inflation, softening of core inflation, improvement in manufacturing capacity utilization, healthy profits, and healthy consumer demand.

On the inflation front, global oil prices have softened, leading to some softening in prices of oil derived products. Categories of food too, are starting to see a moderation in inflation yet remain the key risk to inflation prints. The RBI has revised its GDP growth forecast for India to 7.0% for FY24 from 6.5% earlier.

Recently, the RBI increased the risk weights on loans given by banks to NBFCs and unsecured personal loans given out by NBFCs. This could lead to an increase in interest rates of certain categories of unsecured retail loans. With this, the RBI has effectively delivered a very targeted rate hike for loans where it seeks the risks to be concentrated. With these regulations, lenders are expected to take precautionary measures to limit their exposure to unsecured retail lending, as observed over the last few months, with on-year growth under secured retail loans averaging 33% in Q2 FY24, compared to 26% under unsecured retail loans.

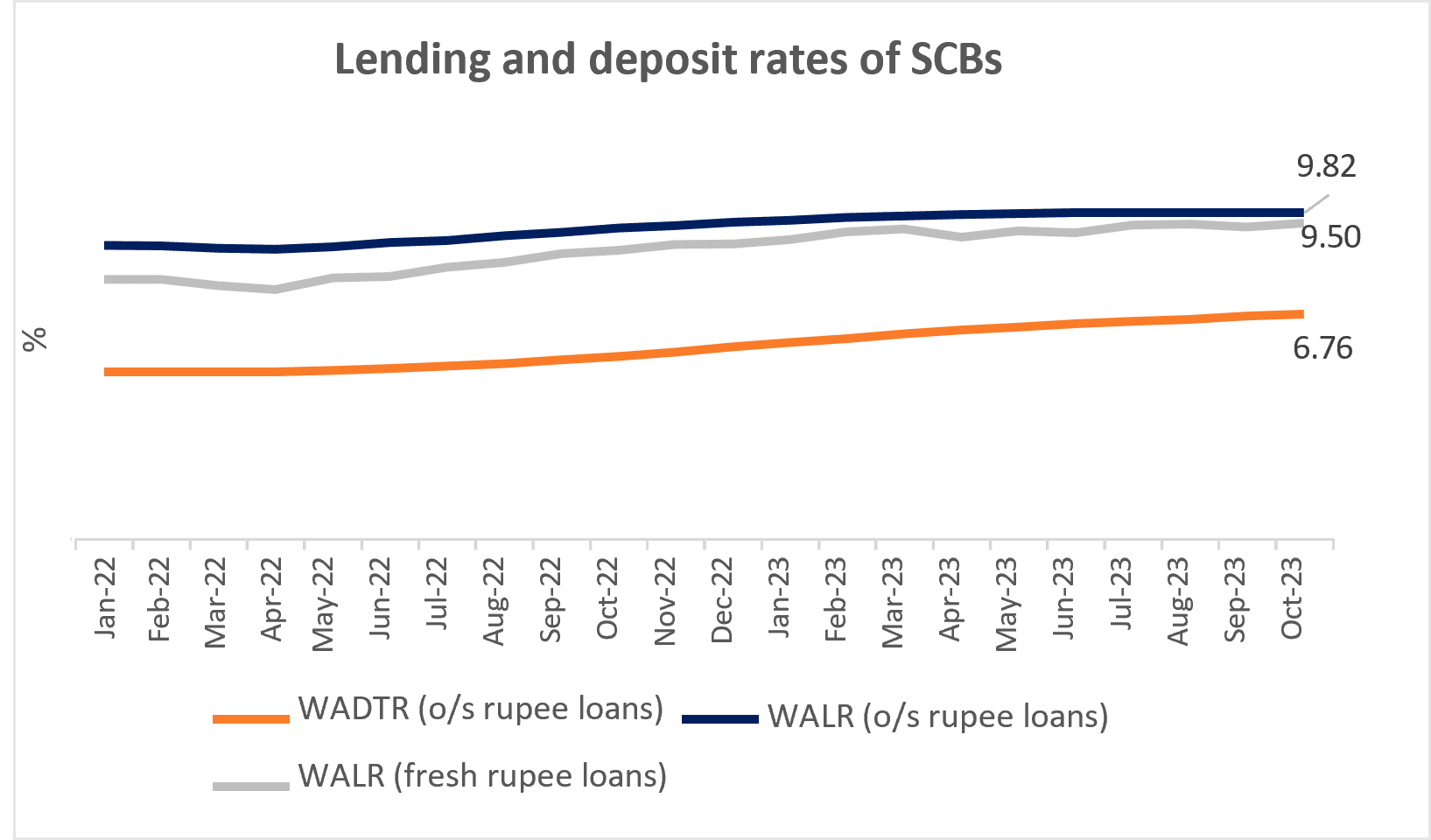

Despite rate hikes throughout FY23, real GDP grew 7.6% on-year in the quarter-ended Sep’23 compared to 7.8% in the previous quarter. While the repo rate increased by 250bps, WALR on fresh rupee loans has increased by only 200bps. Investment as a share of GDP for Q2 FY24 stood at 35.3% vs 34.7% the previous quarter and a long-term average of 31.8% (FY14-FY23). Steady/softening interest rates, easing inflation, healthy demand, and rising levels of capacity utilization, bode well for the growth story in the coming quarters.

HeadlineCPIhassubsidedoverthelastfewmonths,withonlyone-thirdofitemsintheCPIbasketexperiencinginflationof6%or above,comparedtoone-halfinFeb’23.TheIMFinitslatestWorldEconomicOutlookreport,predictstheIndianeconomytogrowby 6.3%in2024andtheRBItooexpectstheeconomytodobetterthanbefore.FOMCmemberChristopherWallerrecentlysignaled the possibilityofratecutsin2024,providedtheU.S.CPIinflationloweredforfewmoremonths.Comfortinginflation,healthyreal economy and a rate cutbytheU.S. Fed couldset the stage for a ratecutnextyear.However,the RBIisunlikelytooptforarate cut beforetheU.S.Fed.

Wtd. avg. call rates averaged 6.67% in Nov’23

Falling CPI though food inflation remains sticky

Wtd. avg. call rates averaged 6.67% in Nov’23

Falling CPI though food inflation remains sticky

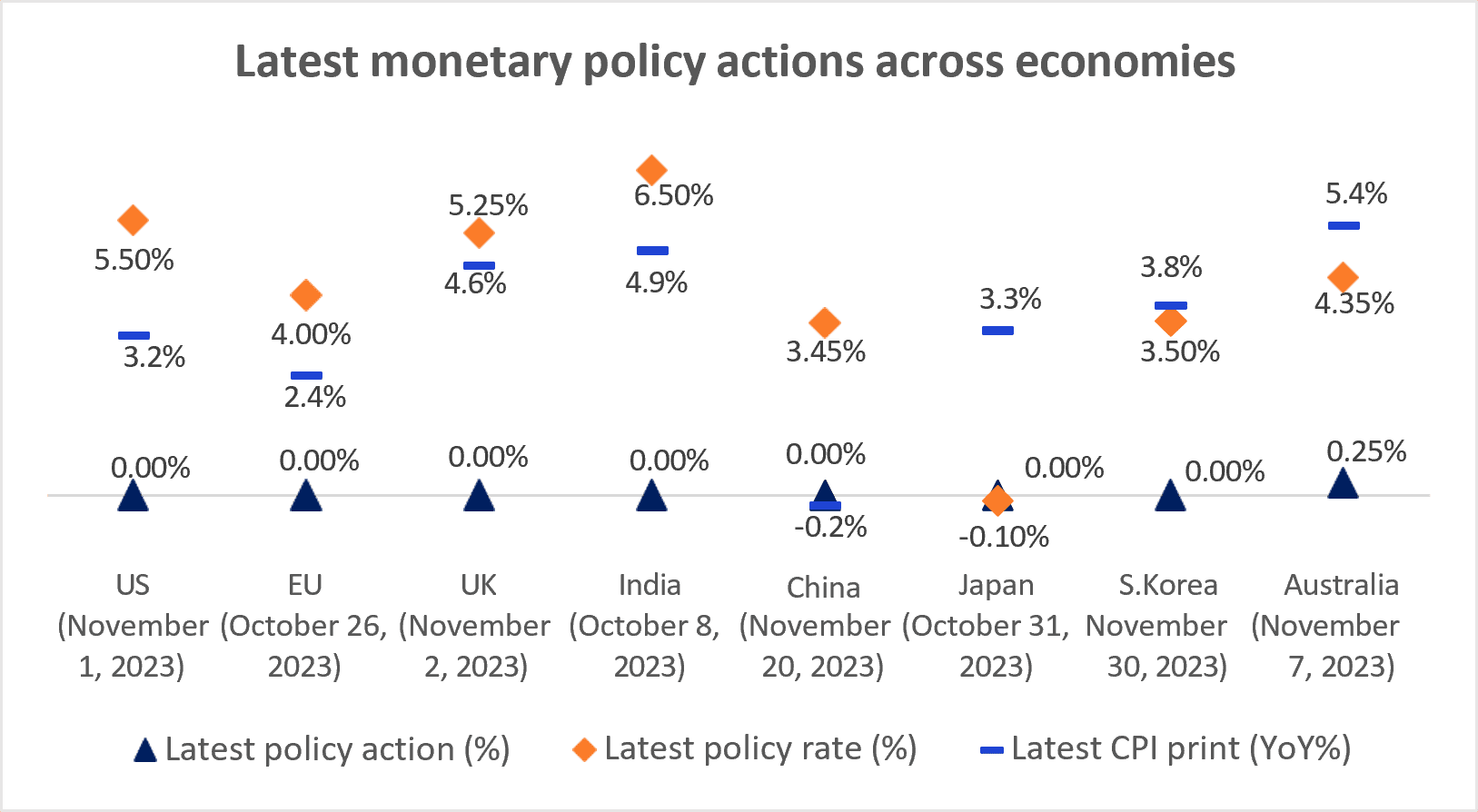

Most central banks are off the rate hike cycle

Sector-wise transmission to WALRs (May’22-Sep’23)

Most central banks are off the rate hike cycle

Sector-wise transmission to WALRs (May’22-Sep’23)

Transmission of rate hikes still underway

Around 30% of CPI basket experiencing >6% inflation

Transmission of rate hikes still underway

Around 30% of CPI basket experiencing >6% inflation

Yield differential has narrowed

SCB credit grew 19.8% in Q2 FY24 vs 15.8% in Q1 FY24

Yield differential has narrowed

SCB credit grew 19.8% in Q2 FY24 vs 15.8% in Q1 FY24

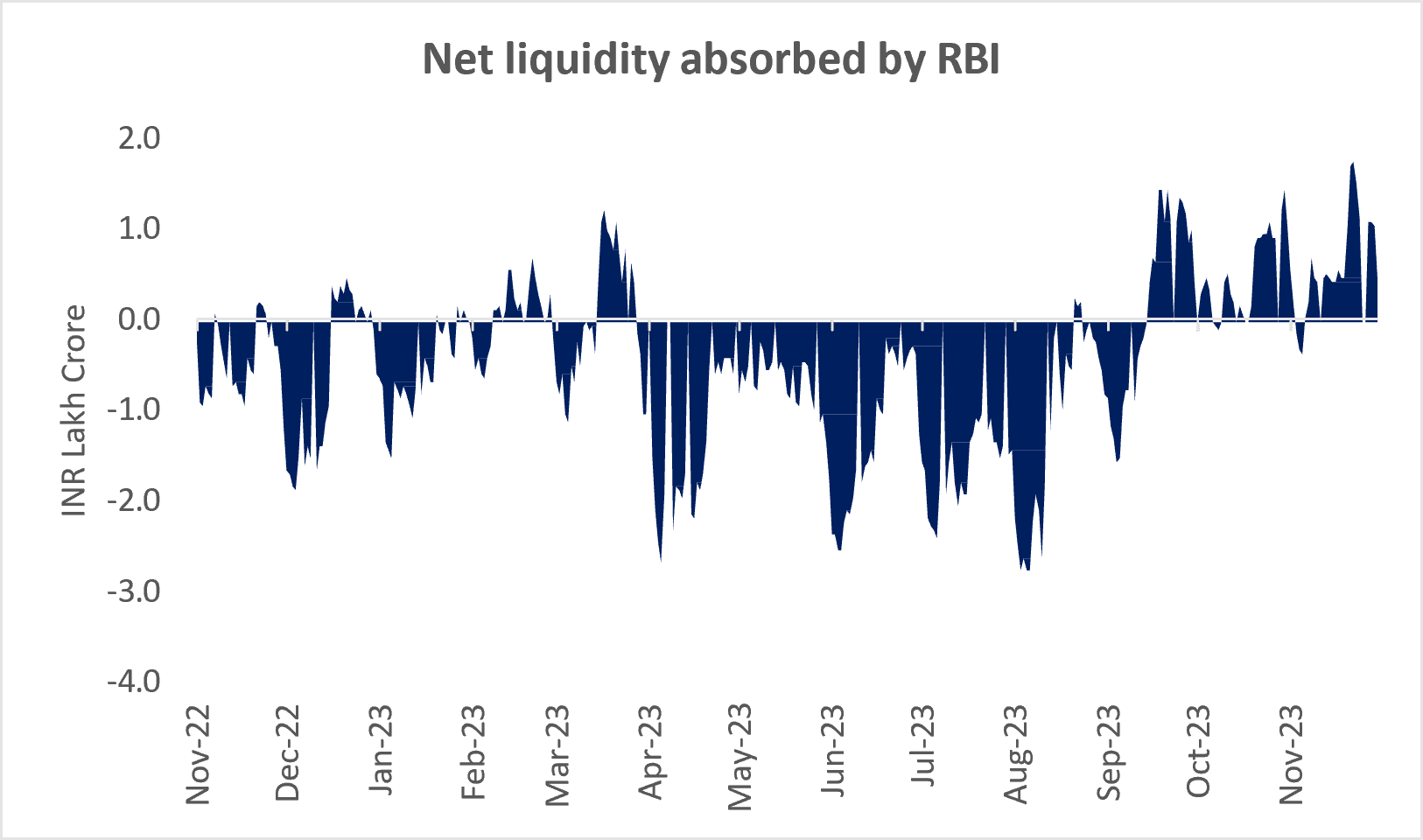

Liquidity deficit since last three months

Rise in unsecured retail loans outstanding by SCBs

Liquidity deficit since last three months

Rise in unsecured retail loans outstanding by SCBs

TruQuest is knowledge series launched by TruBoard Partners providing succinct updates and views on:

Liquidity outlook

India’s macro economic view

Trends within the infrastructure, Real Estate and Renewable Energy sectors

Impact analysis of new regulations and policies on lending and capital flow

Anuj Agarwal, Chief Economist Ria Rattanpal, Research Associate

Author:

Anuj Agarwal, Chief Economist Ria Rattanpal, Research Associate

Disclaimer

The data and analysis covered in this report of TruQuest has been compiled by TruBoard Pvt Ltd and its associates (TruBoard) based upon information available to the public and sources believed to be reliable. Though utmost care has been taken to ensure its accuracy, no representation or warranty, express or implied is made that it is accurate or complete. TruBoard has reviewed the data, so far as it includes current or historical information which is believed to be reliable, although its accuracy and completeness cannot be guaranteed. Information in certain instances consists of compilations and/or estimates representing TruBoard’s opinion based on statistical procedures, as TruBoard deems appropriate. Sources of information are not always under the control of TruBoard. TruBoard accepts no liability and will not be liable for any loss of damage arising directly or indirectly (including special, incidental, consequential, punitive or exemplary) from use of this data, howsoever arising, and including any loss, damage or expense arising from, but not limited to any defect, error, imperfection, fault, mistake or inaccuracy with this document, its content.