Rupee has an appreciating bias, RBI likely to piggy-back on it

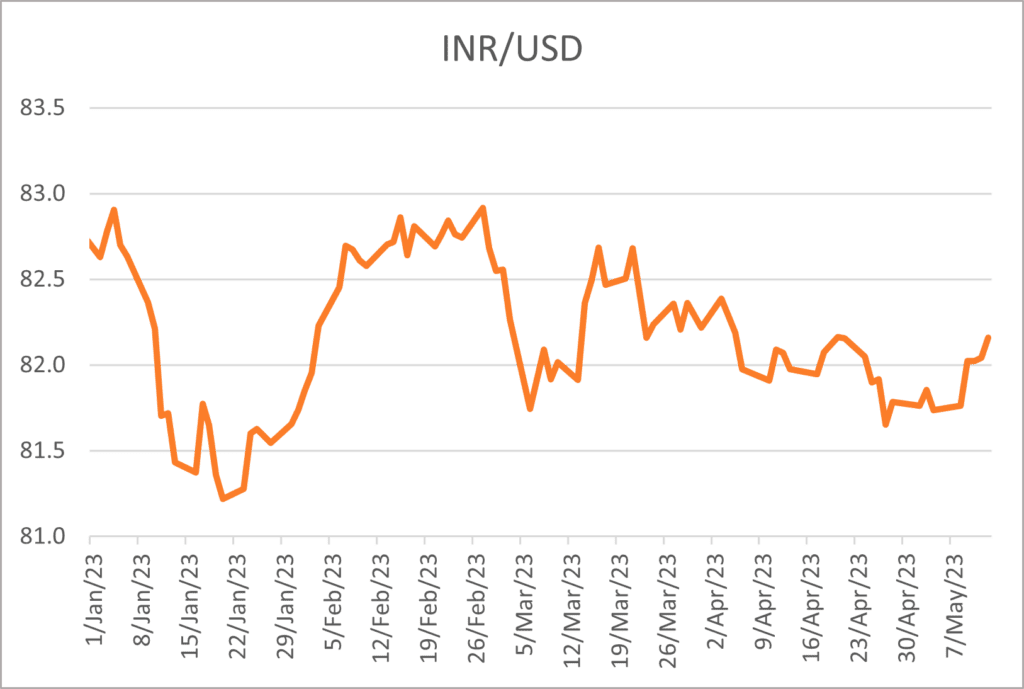

The rupee has appreciated by 0.7% in the first week of May 2023 as compared to end-March 2023 and 1.4% compared to end-December 2022. Broad fundamental reasons have contributed to the recent appreciation of rupee, and these are likely to sustain.

Trade position has improved with merchandise trade deficit coming down and services surplus increasing. The negative impact of weak global growth is likely to be more pronounced on merchandise exports than services exports. For quarter ending March 2023, services surplus is up 45% YoY and 5% QoQ.

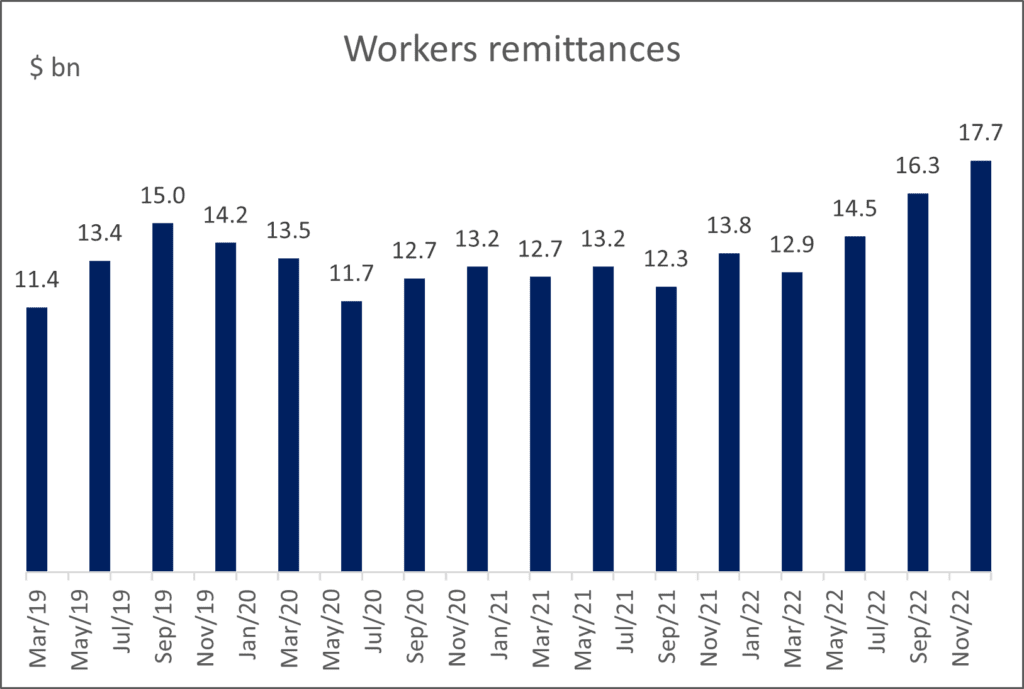

Current account deficit (CAD) for 3QFY23 came in 2.2% of GDP Vs 3.7% in the previous quarter. CAD witnessed a 41% QoQ reduction in 3QFY23. Global commodity prices have softened since September 2022. Concerns over weak exports growth stem from weak economic outlook for the US and EU, which account for over one-third of India’s exports. Despite the COVID-19 pandemic and global lay-offs workers’ remittances have remained steady throughout and are now above pre-pandemic levels.

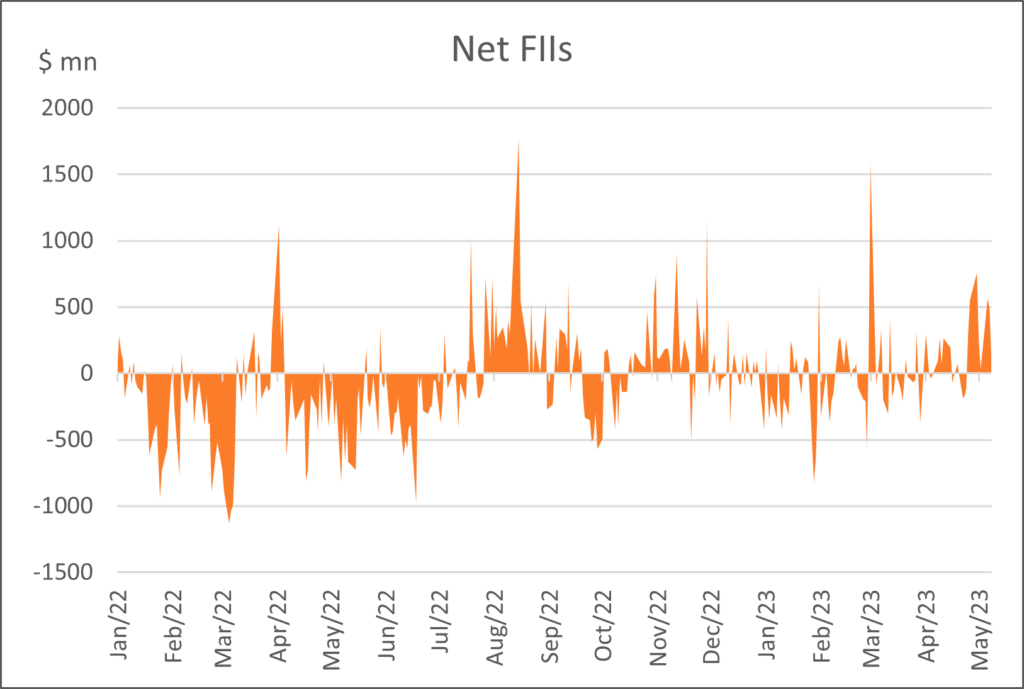

FIIs have turned positive. FIIs have been net buyers in the domestic markets to the tune of $1.6 billion in 2023 so far Vs them being net seller to the tune of $18.5 billion in 2022. Global risk-off sentiments have eased. Foreign direct investment inflows have remained steady and have totaled $36 billion during the first three quarter of fiscal 2023. This is likely to benefit going ahead from PLI schemes and ‘China+1’ sentiment.

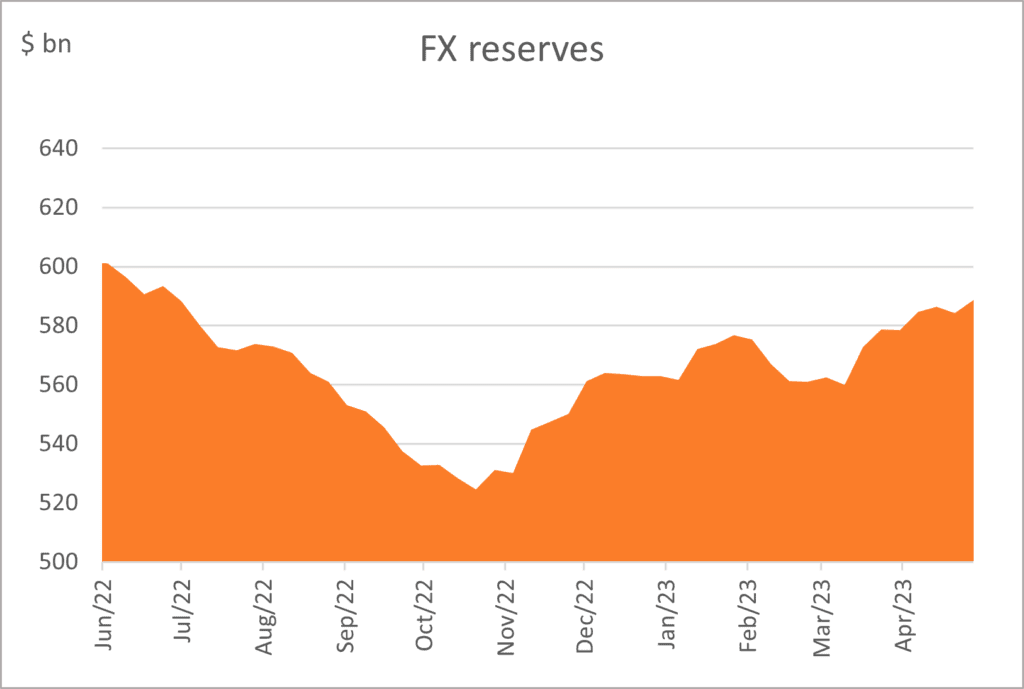

The RBI is shoring up its reserves. FX reserves stood have swelled by $27 billion since the start of 2023. Import cover has improved to 10.6 months in March 2023 from 8.5 months in September 2022.

We feel that rupee has a strengthening bias basis the underlying fundamentals. REER has been falling in the last 6 months reflecting an increase in India’s competitiveness and an appreciating bias for the currency. India remains the fastest growing major economy, and investor interest remains positive. Weak exports will get some cushion from fall in imports (on account of weak domestic growth and benign global commodity prices). India has emerged as the largest importer of sanctioned Russian oil (making up 20% of Indian’s oil imports). Reports suggest that Russian crude is available at a 25-30% discount to the global benchmark. So long as Russia remains under sanctions, India can cushion its import bill with cheap Russian oil.

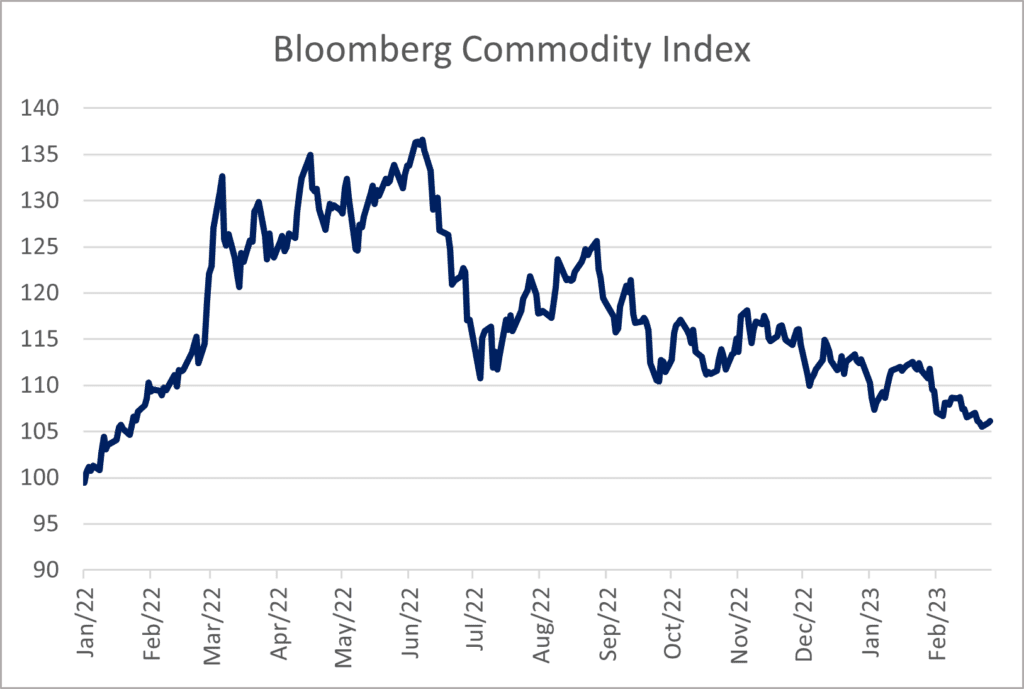

The rise in global oil prices in response to the OPEC+ production cuts announced in April 2023 was short lived. Analysts estimate a global oil deficit in the second half of 2023 which could significantly push up oil prices. However, we feel that concerns over weak global growth will dominate sentiments and keep oil prices contained. This will keep broader commodity inflation in check too.

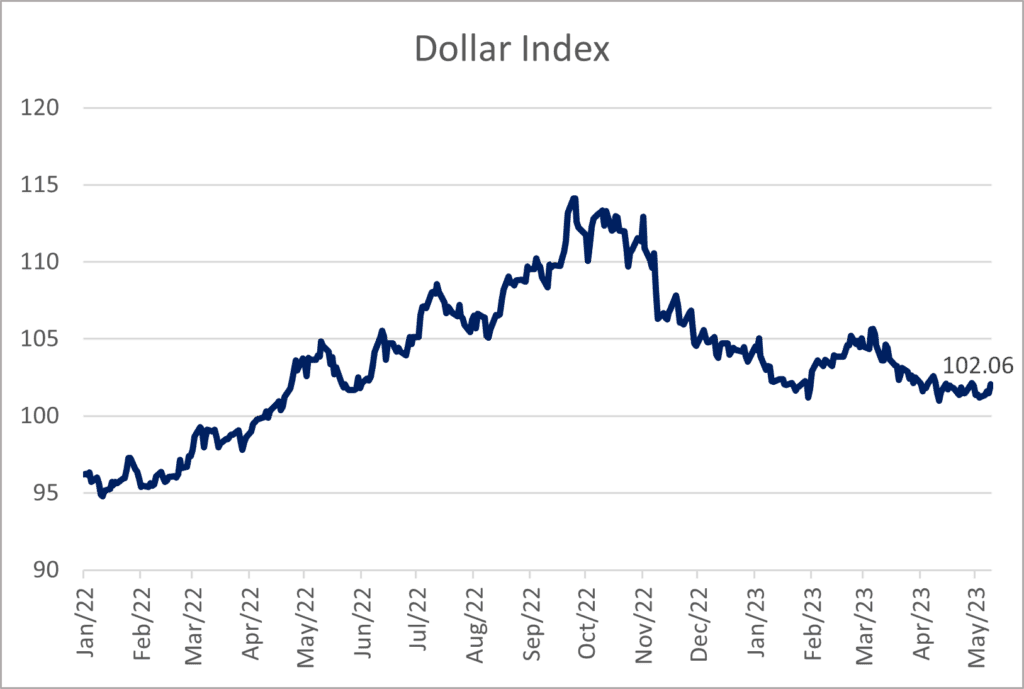

TheUS Fed has hinted at a pause going ahead and most major central banks are likely to follow suit. The US banking crisis, softening inflation and a pause by the Fed will keep dollar’s strength in check.

The RBI is likely to use this opportunity of positive fundamentals to build up its reserves, and at the same time keep Indian exports competitive by keeping the rupee appreciation under check.

Trade balance to support

rupee

Investor sentiment turns

positive

Liquidity surplus has reduced

significantly

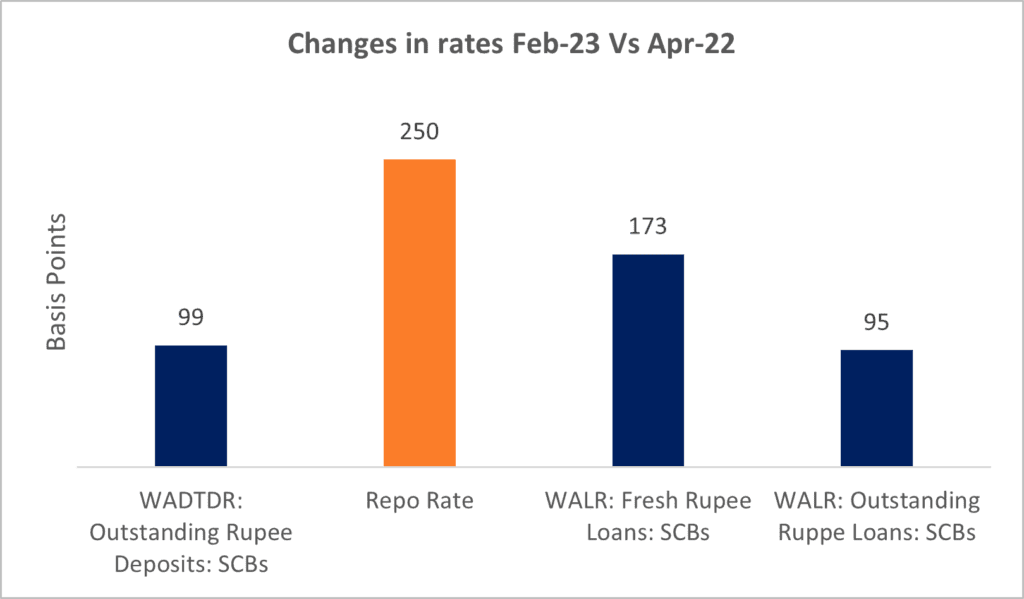

Transmission of past hikes is

slow

Remittances have remained strong despite COVID and global lay-offs

CAD remains in a comfortable

position

RBI revises its GDP growth forecast

upwards

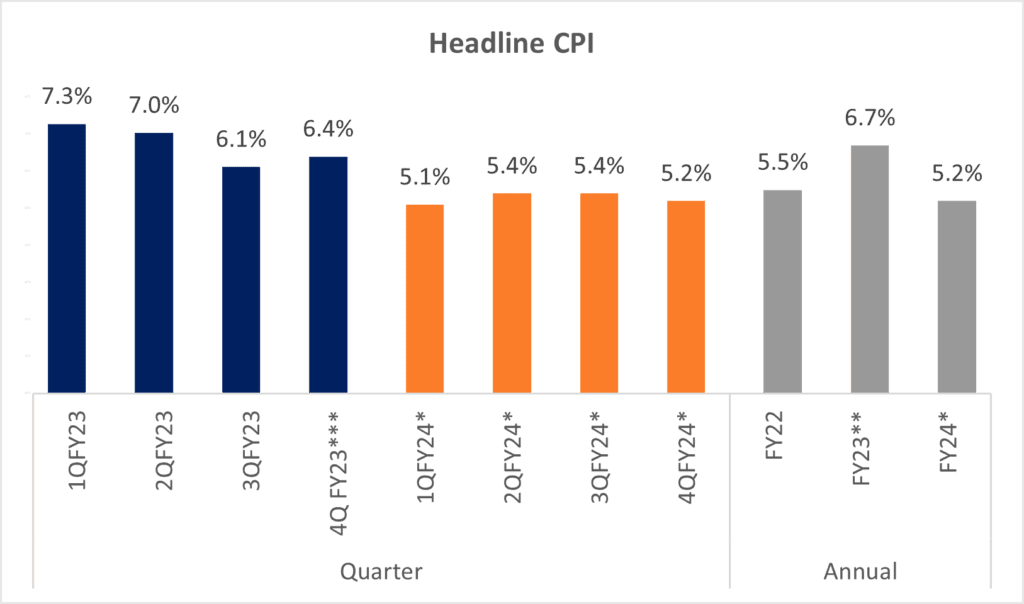

Inflation forecast is revised

downwards

INR is among the better performing currencies in 2023 with low volatility

Falling REER signals an appreciating bias for

INR

Real Repo Rate still below pre-pandemic levels

levels

RBI seems to be on the optimistic

side

RBI has been shoring up its

reserves

Commodity prices have been on a

downtrend

With a weak economic outlook and Fed pause, US dollar is losing its strength

CAD remains in a comfortable

position

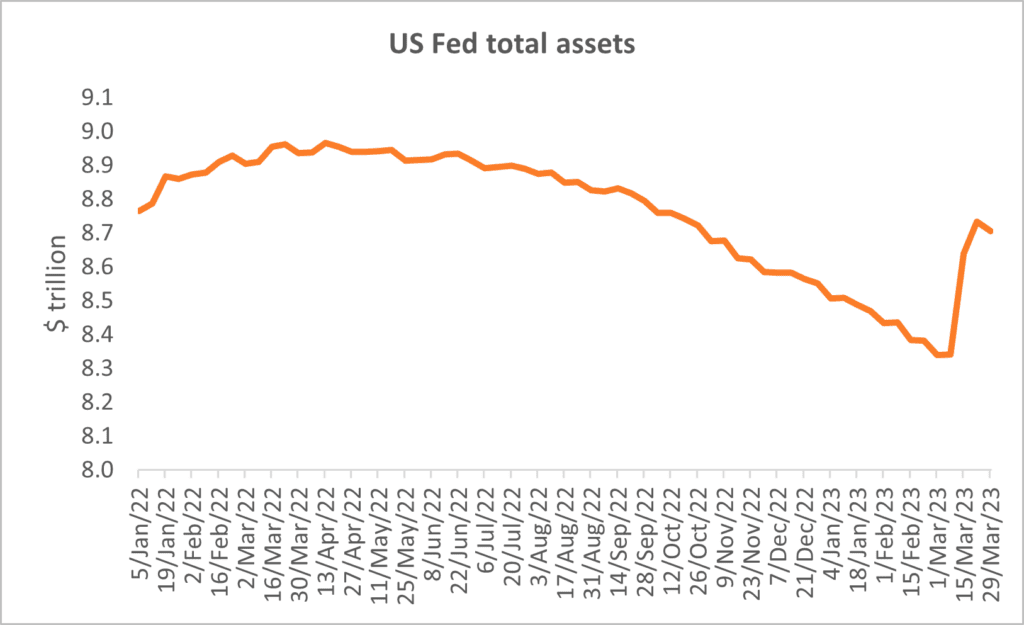

US Fed is increasing its balance

sheet

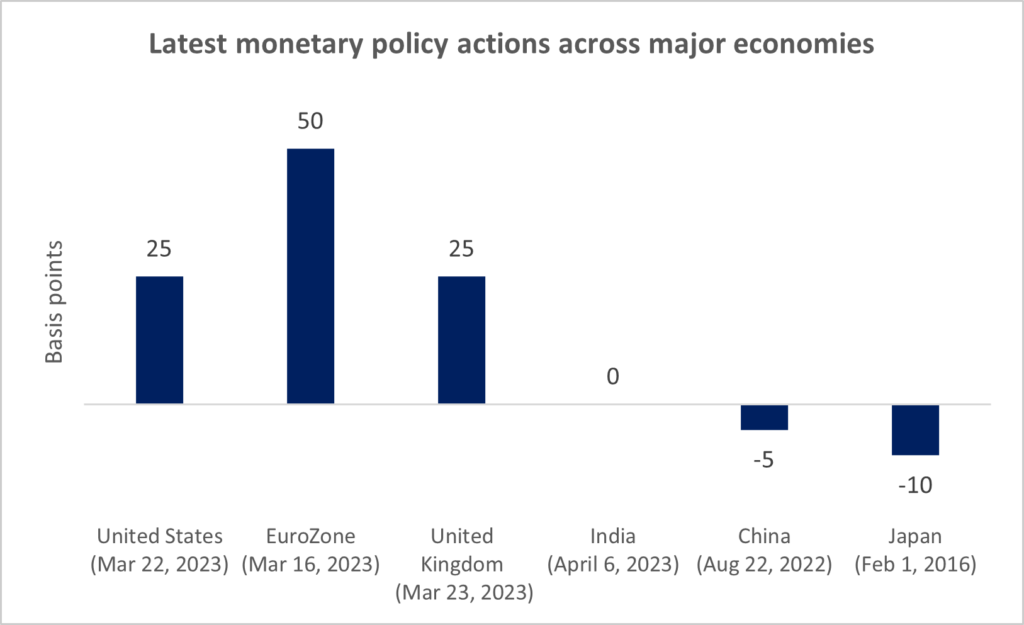

Some hike, some don’t

.

TruQuest is knowledge series launched by TruBoard Partners providing succinct updates and views on:

Liquidity outlook

India’s macro economic view

Trends within the infrastructure, Real Estate and Renewable Energy sectors

Impact analysis of new regulations and policies on lending and capital flow

Anuj Agarwal, Chief Economist Ria Rattanpal, Research Associate

Author:

Anuj Agarwal, Chief Economist Ria Rattanpal, Research Associate

Disclaimer

The data and analysis covered in this report of TruQuest has been compiled by TruBoard Pvt Ltd and its associates (TruBoard) based upon information available to the public and sources believed to be reliable. Though utmost care has been taken to ensure its accuracy, no representation or warranty, express or implied is made that it is accurate or complete. TruBoard has reviewed the data, so far as it includes current or historical information which is believed to be reliable, although its accuracy and completeness cannot be guaranteed. Information in certain instances consists of compilations and/or estimates representing TruBoard’s opinion based on statistical procedures, as TruBoard deems appropriate. Sources of information are not always under the control of TruBoard. TruBoard accepts no liability and will not be liable for any loss of damage arising directly or indirectly (including special, incidental, consequential, punitive or exemplary) from use of this data, howsoever arising, and including any loss, damage or expense arising from, but not limited to any defect, error, imperfection, fault, mistake or inaccuracy with this document, its content.