RBI pauses, keeps stance unchanged at “withdrawal of accommodation”

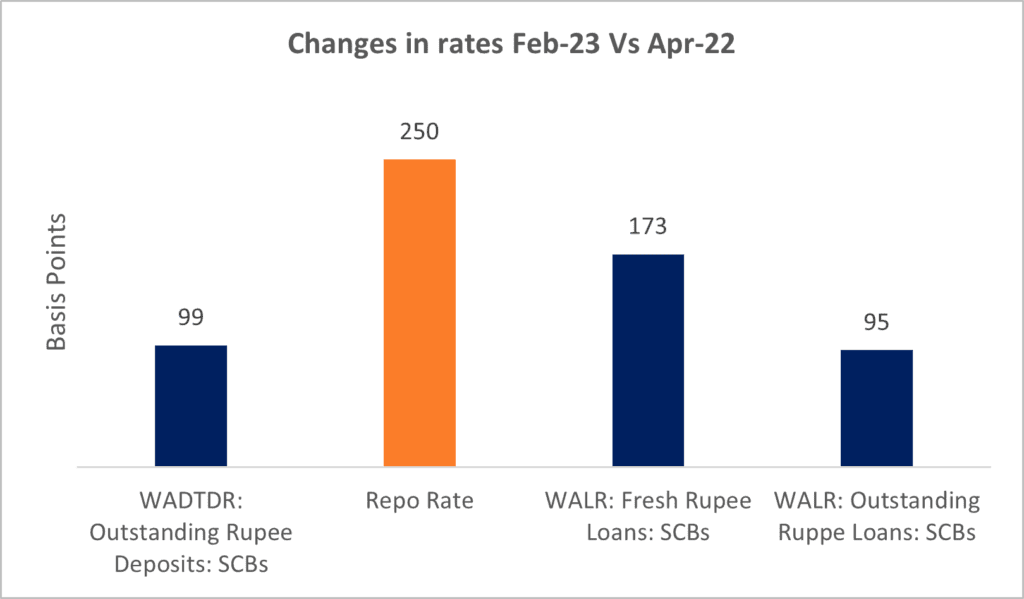

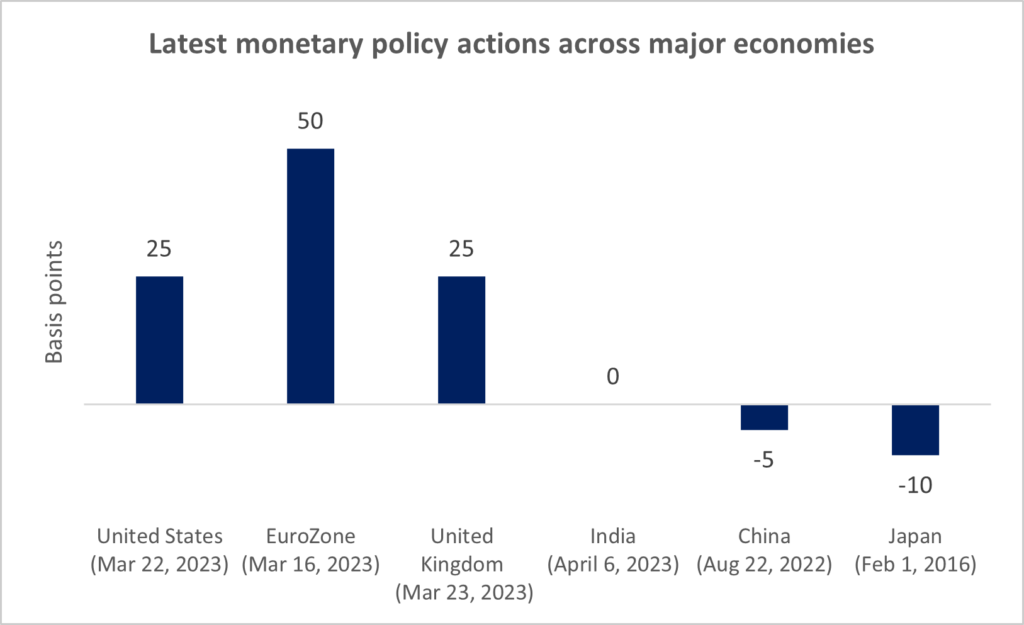

The Reserve Bank of India’s monetary policy committee (MPC) kept the repo rate unchanged at 6.5% against an expected 25 bps hike in its April 2023 meeting. Our expectation was a hike this time and then pause, especially after the US fed hiked rates by 25 bps last month. RBI’s move seems to have been guided by recent developments – banking crisis in Europe and the U.S., interventions by the Fed to support U.S. banks, increasing concerns over slowing global growth (which will have negative spill overs on to India), and a cooling inflation. The Reserve Bank of Australia too held its rates steady in its policy statement on 4th April 2023, citing its needs to assess the impact of past hikes (360 bps) and evolving economic scenario. The RBI has already increased repo rate by a total of 250 bps since May’2022, and that is yet to fully transmit through the system.

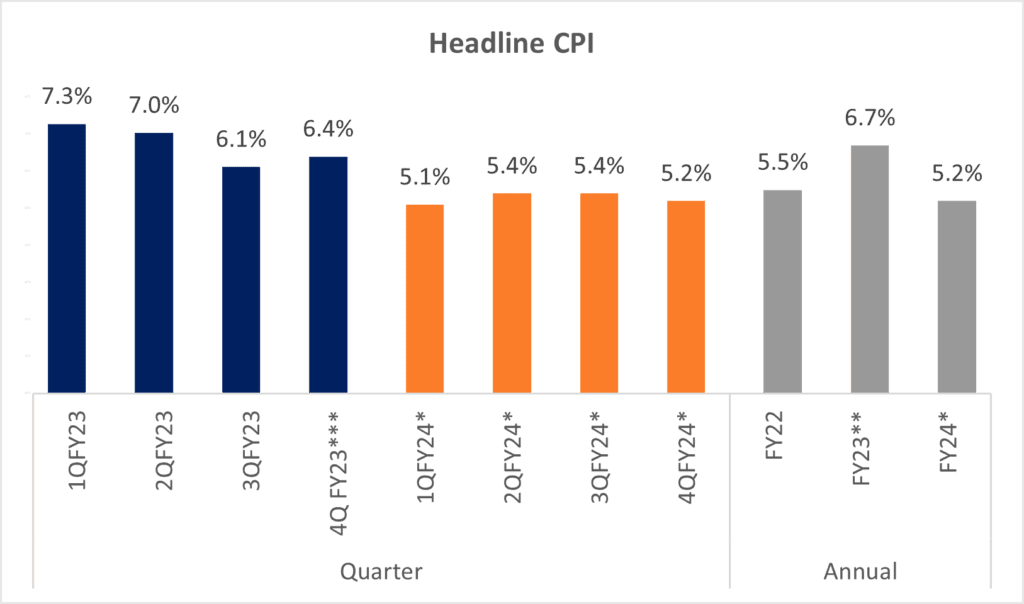

The RBI raised GDP growth forecast for India in FY24 from 6.40% to 6.50%. This seems a bit optimistic and much higher than median of professional forecasters. On assumption for oil too at $85/bbl, the RBI seems to be optimistic as compared to the market. With the recent output cuts announced by OPEC+, many analysts believe that oil could easily touch $100 in the next couple of months. Inflation forecasts by the RBI have been lowered from 5.3% to 5.2% for FY24.

Going ahead, monetary tightening is expected to come in the form of reduced liquidity in the system. Liquidity surplus has come down significantly. Additionally, long term durable liquidity worth ~Rs 73,000 crores provided under long term repos in the COVID years is due for maturity in March and April of 2023. The RBI is likely to hold rates steady for now. While the RBI has stated its stance as ‘withdrawal of accommodation’ and said it would not refrain from taking further action if required, a hike is highly unlikely in the next policy meeting. WPI inflation has cooled significantly in the last 6 months coming in at 3.9% for February’2023. CPI inflation too will start easing in the coming months as the high base effect starts to kick-in. The past rate hikes too are yet to be fully absorbed by the banking system. Moreover, a pause now and a hike in the next policy might be perceived as a volatile move. With CPI expected to moderate, and most DM central banks at the end of their rate hike cycle, the RBI will need a very strong case to push for a hike. A rate cut too seems farfetched unless developed market central banks (US Fed, ECB, BoE) do something similar in their next policy moves, on unexpected lines.

Liquidity surplus has reduced

significantly

Transmission of past hikes is

slow

Liquidity surplus has reduced

significantly

Transmission of past hikes is

slow

RBI revises its GDP growth forecast

upwards

Inflation forecast is revised

downwards

RBI revises its GDP growth forecast

upwards

Inflation forecast is revised

downwards

*Estimates by the RBI in April 2023

*Estimates by the RBI in April 2023, **Data from Apr’22-Feb’23 *** Data taken for Jan and Feb’23

Real Repo Rate still below pre-pandemic levels

levels

RBI seems to be on the optimistic

side

Real Repo Rate still below pre-pandemic levels

levels

RBI seems to be on the optimistic

side

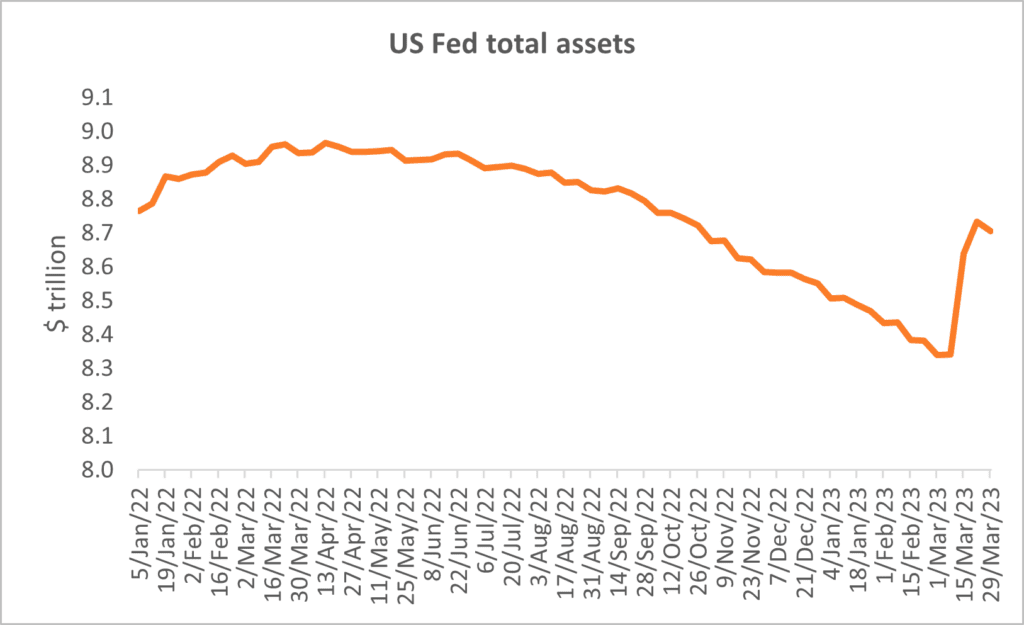

US Fed is increasing its balance

sheet

Some hike, some don’t

.

US Fed is increasing its balance

sheet

Some hike, some don’t

.

Source: OPEC, IEA, EIA, CEIC, PPAC, BP, TruBoard

TruQuest is knowledge series launched by TruBoard Partners providing succinct updates and views on:

Liquidity outlook

India’s macro economic view

Trends within the infrastructure, Real Estate and Renewable Energy sectors

Impact analysis of new regulations and policies on lending and capital flow

Anuj Agarwal, Chief Economist Ria Rattanpal, Research Associate

Author:

Anuj Agarwal, Chief Economist Ria Rattanpal, Research Associate

Disclaimer

The data and analysis covered in this report of TruQuest has been compiled by TruBoard Pvt Ltd and its associates (TruBoard) based upon information available to the public and sources believed to be reliable. Though utmost care has been taken to ensure its accuracy, no representation or warranty, express or implied is made that it is accurate or complete. TruBoard has reviewed the data, so far as it includes current or historical information which is believed to be reliable, although its accuracy and completeness cannot be guaranteed. Information in certain instances consists of compilations and/or estimates representing TruBoard’s opinion based on statistical procedures, as TruBoard deems appropriate. Sources of information are not always under the control of TruBoard. TruBoard accepts no liability and will not be liable for any loss of damage arising directly or indirectly (including special, incidental, consequential, punitive or exemplary) from use of this data, howsoever arising, and including any loss, damage or expense arising from, but not limited to any defect, error, imperfection, fault, mistake or inaccuracy with this document, its content.