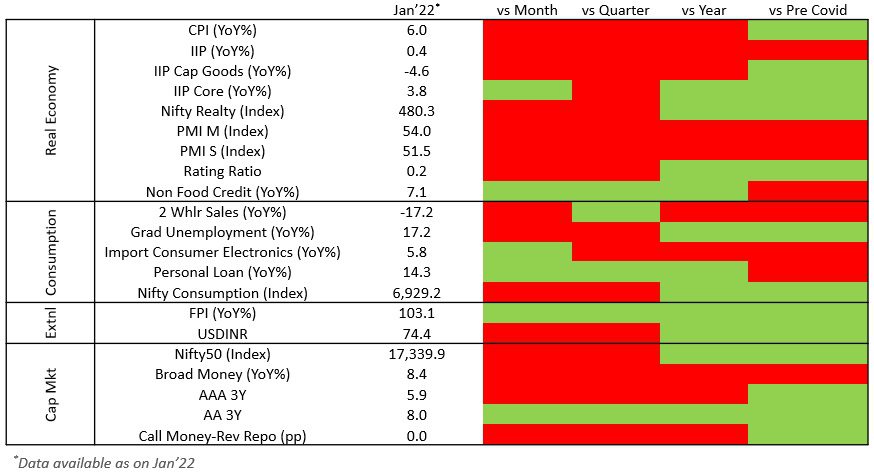

- India’s lockdown intensity, as measured by University of Oxford, was 84 by end of Jan’22, compared to 56 in US, 42 in UK, 62 in Brazil and 42 in South Africa.

- Indian economic recovery remained subdued in Jan’22. Strict lockdowns, despite localized, had a severe impact on day-to-day economic activity culminating into weakening macro indicators.

- Industrial units, especially MSMEs, are running with significantly low levels of capacity utilization, employment levels and productivity as measured by Index of Industrial Production (IIP). Heavy wholesale and retail price inflation and interest expenses coupled with low sales are squeezing margins for manufacturers.

- While exporting industries remain a beacon of hope, rising global competition, high raw material prices and expensive capital could become severe impediments unless supported with judicious fiscal policy interventions.

- The building stresses within real economy are mirrored in the capital markets, especially the debt market. Surging yield spreads, decoupling with RBI’s signaling, rising costs of borrowing and volatile equity markets are early warning signals of upcoming financial stress.

Source: TruBoard Research, CMIE, Oxford University Lockdown Stringency Index

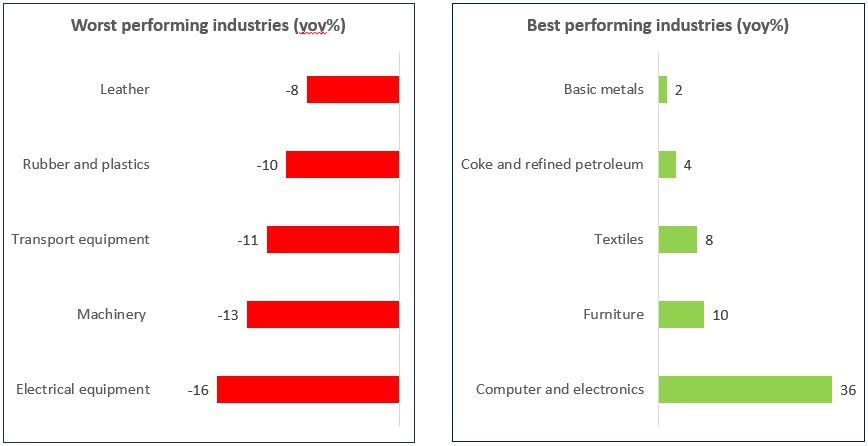

- Government estimates suggest manufacturing activity shrunk by 0.14% in Dec’21 (YoY). The sector has been slowing down once again since Aug’21.

- A slowdown in manufacturing has set off a vicious economic cycle owing to its contribution to GDP (20%) and employment (26%). Quick policy support is required to reinvigorate India’s MSMEs (driving manufacturing and employment) to restore them to pre-2017 levels. (Indian economy has been on a steady slowdown since 2017)

- Government estimates further suggest persistent slowdown in production of machineries and heavy equipment (see chart), which is a fallout of reduced private capex. Lack of business expansion will not only take a toll on employment and growth but will also lead to a fresh round of nonperforming assets related problem within the fragile financial system. At a time when liquidity (global and domestic) is expected to dry, such risks can quickly turn into a contagion of bankruptcies and insolvencies.

- A sharp rise in global demand, especially in USA and UK (pent up demand) and a China+1 strategy adopted by global manufacturers presents an opportunity for Indian merchandise exporters. Swift policy support and short-term regulatory forbearances can help them capitalize this momentary window of opportunity.

Source: TruBoard Research, CMIE, Oxford University Lockdown Stringency Index

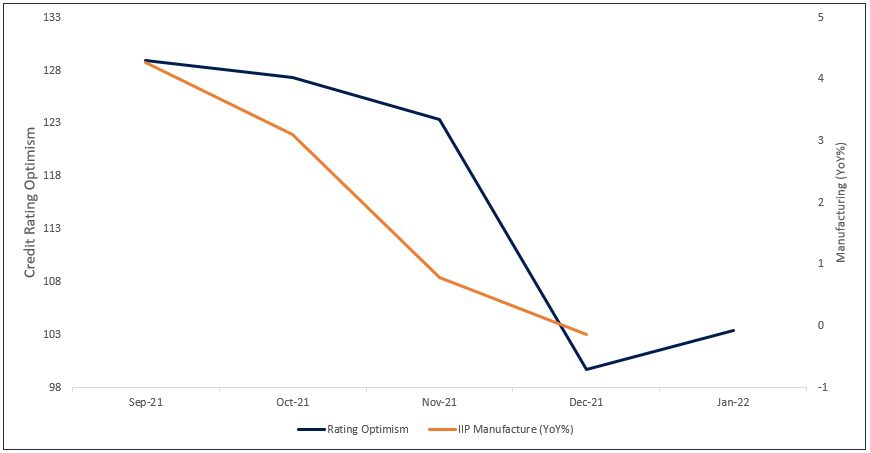

- The TruBoard Rating Optimism measures the rise or fall in optimism among major rating agencies, compared to a base period (Jun’17). Empirical analysis suggest rating outlook serves as an early warning signal for economic activity.

- There is a strong causality between the Index (lead) and industrial production (manufacturing) levels in India. The marginal uptick in the Rating Index in Jan’22, if sustained, can be an early sign of a possible recovery in manufacturing in Q4 FY22.

Source: TruBoard Research, CMIE, Oxford University Lockdown Stringency Index