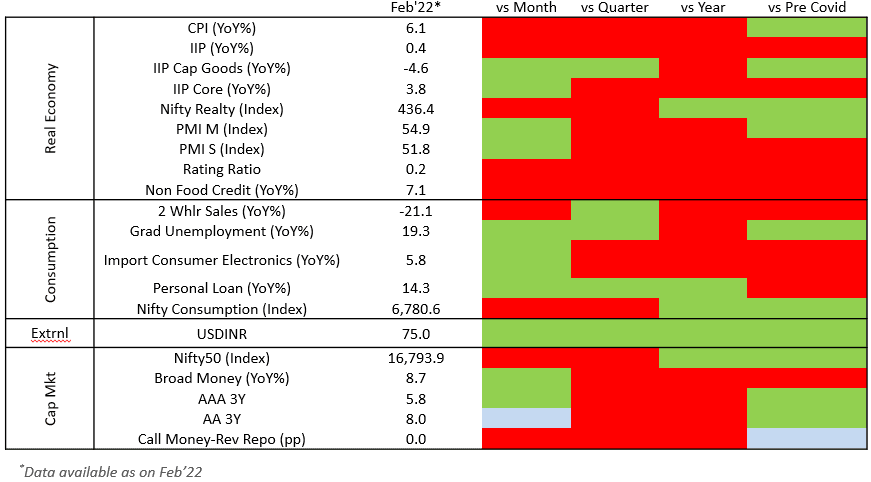

- Global economy witnessed a synchronous recovery in Feb’22 as Omicron infections subsided and lockdown intensities eased. India was no exception as depicted by the rising greens in the chart above.

- However, the Ukranian conflict threatens global economic stability driven by collapsing supply chains, rising commodities and agricultural prices and capital flight. We anticipate a weaker heatmap (more reds) in the coming months.

- In the first 15 days of Mar’22, Indian capital markets witnessed a net outflow of ~USD 6 bn of foreign investments, compared to an outflow of USD 3.8 and USD 5 bn respectively in Jan’22 and Feb’22, thereby weakening USDINR. Recent reports suggest Reserve Bank of India’s interventions amounting to ~USD 10 bn to reduce USDINR’s volatility.

- Western sanctions on Russian energy exports and the fear of wheat and edible oil shortages is driving inflation globally, including in India. This will have a negative impact on global and local aggregate demand thus adding to the woes of Indian producers and exporters in the short to medium term.

- Lower export and local demand, coupled with higher raw material prices, wage inflation and higher interest costs can be a threat on the asset quality of lenders, over and above the existing risks.

Source: TruBoard Research, CMIE, Oxford University Lockdown Stringency Index

- India’s Industrial production grew by a meagre 1.3% in Jan’22 (compared to a year back). One of its components, capital goods, shrunk by 1.4% , suggesting lingering weaknesses in private capex.

- Despite public policy-based efforts to ensure smooth availability of working capital to a large section of MSMEs, capital expenditure by India Inc remains on the back burner due to skepticism around future demand. High cost of capital is another pull back. The Ukraine war further blurred the visibility on demand revival in near future.

- We expect continued monetary policy support to ensure undisrupted credit flow to MSMEs despite the growing risks on inflation. In addition, fiscal policy support to public capex needs to be frontloaded in FY23. Also, higher revenue expenditure is desirable to address the dual menace of virus and war on the common Indian masses.

Source: TruBoard Research, CMIE, Oxford University Lockdown Stringency Index

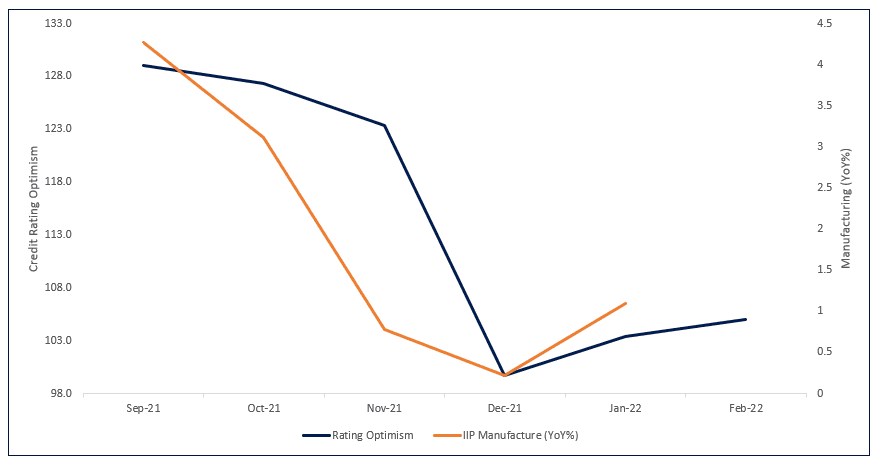

- Manufacturing activity (IIP-Manufacture) is mimicking the trend charted by the TruBoard Index. The Index had predicted a better manufacturing data for Jan’22 compared to the previous month. The Index now predicts that manufacturing in Feb’22 data is expected to remain positive though with a slight moderation. Early estimates of the Index in Mar’22 suggests a slowdown in manufacturing activity as explained in the commentary above. Government data for Mar’22 manufacturing will be available in May’22.

- The strong correlation is guided by the fact that the TruBoard Index captures sentiment of rating agencies on MSMEs, which is the driving force behind Indian manufacturing.

Source: TruBoard Research, CMIE, Oxford University Lockdown Stringency Index