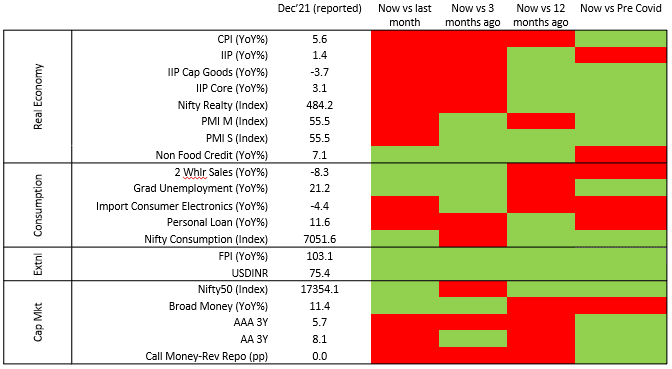

- The heat-map is skewed towards red, suggesting slipping economic activity in recent times.

- While economic activity appears better than what it was before the onset of Covid (Dec’19), high frequency macro indicators have been slowing down sequentially since Oct’21. This is in sync with rising lockdown stringency as Omicron wave intensifies with more than 250,000 daily infections reported across the country.

- Real economy is showing renewed stress with industrial production, capital expenditure as well as construction activity slowing down between Nov-Dec’21.

- Sticky inflation, rising interest rates and high unemployment levels among graduates is further pushing back a consumption led recovery.

- Shrinking two-wheeler sales indicate slowing rural spending, at a time when reverse migration (urban to rural) is picking up with agricultural employment rising to 38% from 35% of total employment, over last 3 years.

- Capital markets are mirroring this stress through rising yields in anticipation of prolonged inflationary pressures. Bank lending remains tepid as private capex fails to pick up. A steady rise in currency in circulation and deposits corroborate weak sentiment towards spending and investments.

Source: TruBoard Research, Centre for Monitoring Indian Economy (CMIE), National Stock Exchange (NSE)

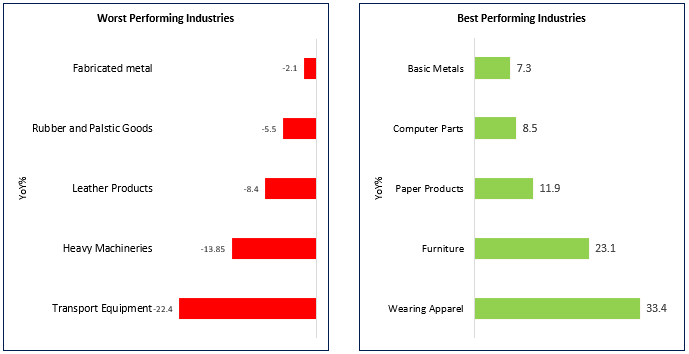

- Latest industrial production data suggest activity fell to an 8 month low of 1.4%.

- Prolonged aversion towards capex have led to a sequential decline in production of machineries and equipment as well as finished metal.

- Global demand however have ensured a steady rise in export industries like textiles and furniture.

- MSMEs which dominate manufacturing continues to face high stress due to rising inventories, steep raw material costs as well as lower domestic demand. The situation is further exacerbated by rising borrowing costs.

- More than 40% of investment projects that were stalled in the first 3 quarters of FY22 belonged to the private sector. Number of private projects dropped rose by 18% in FY22 (YTD) compared to same time in FY20.

- Government support in the form of credit guarantees, cheap liquidity and public capex would be required for a longer period to revive MSMEs which account for 30% of GDP.

Source: TruBoard Research, CMIE, Oxford University Lockdown Stringency Index

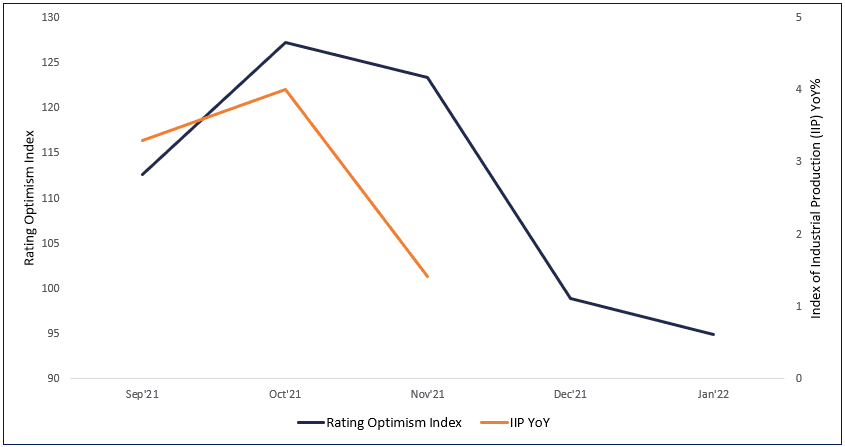

- The TruBoard Rating Optimism measures the rise or fall in optimism among major rating agencies, compared to a base period (Jun’17). Empirical analysis suggest rating outlook serves as an early warning signal for economic activity.

- There is a strong causality between the Index (lead) and industrial production levels in India. Based on the decline in rating optimism in recent months, it is unlikely that industrial production levels will witness any major recovery at least till Jan’22 (government estimates will be available in Apr’22).

- However, as the omicron wave plateaus and starts to subside by end of Jan’22, economic activity is expected to revive once again by early-mid Feb’22, sparking off a renewed bout of growth.

Source: TruBoard Research, CMIE, CRISIL, ICRA